Insolvency by the Numbers #65: NZ Insolvency Statistics May 2026

12 June 2026

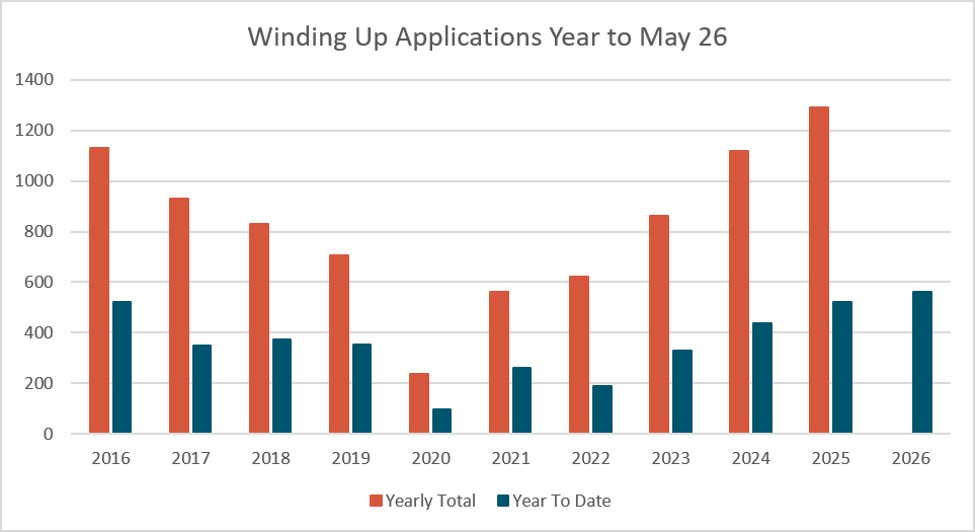

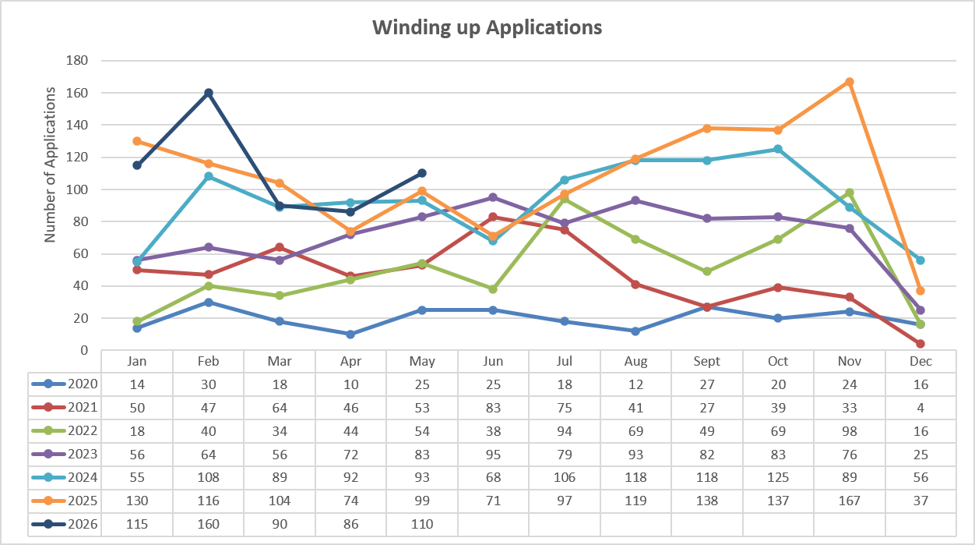

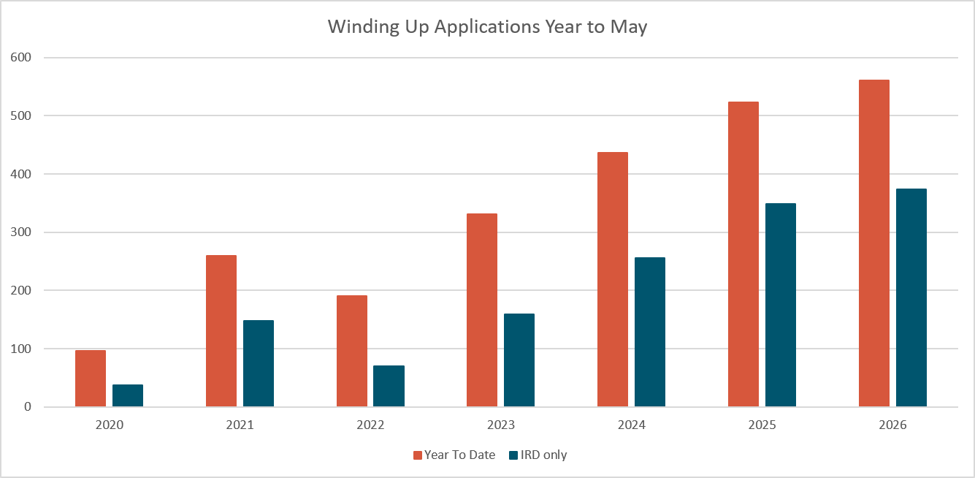

Winding Up Applications

An interesting month for winding up notices. Historically May is a slower months one where the status quo is maintained and notice levels tend to flatten out until July where they start to grow again toward the end of the year.

In May 2026 we did see 110 notices in the month, higher than any previous May’s since 2016 where we saw 116 in the month.

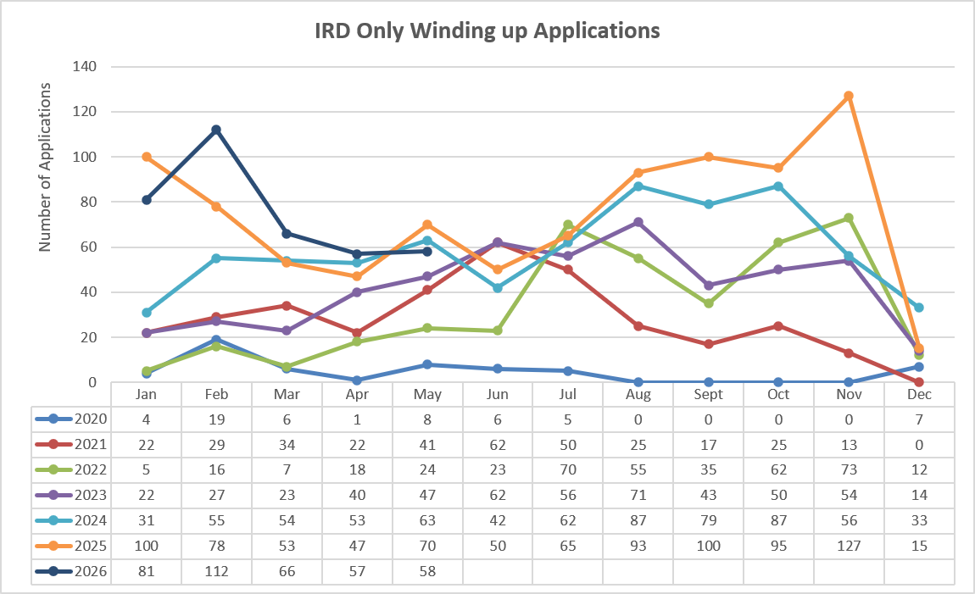

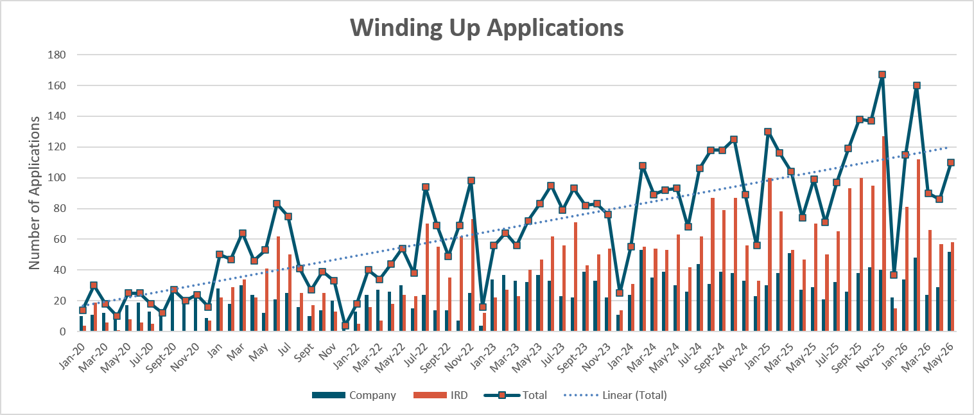

The key difference here on past years has been the early drop off in IRD advertised notices. This could be for a number of reasons:

- Public holidays (Kings birthday) being observed on 1 June would drop notices around this time as people take long weekends,

- The growing tax obligation are now under control – unlikely

- Higher appointments in the shoulder months so a slower May – doesn’t appear to be the case

- Getting the hard word from the government of the day to lay off in the lead up to the election – time will tell on this one

- Very active non-IRD creditors for the month advertising 2x the normal level of appointments for May.

In this instance we see a combination of reduced IRD notices added to non IRD creditors advertising double their usual appointment to give a reasonable high for this time of year, and representing work for insolvency practitioners in the months to come from court appointments.

Year on year 2026 remains the highest number of notices advertised to date indicating we are still on track to exceed 2025.

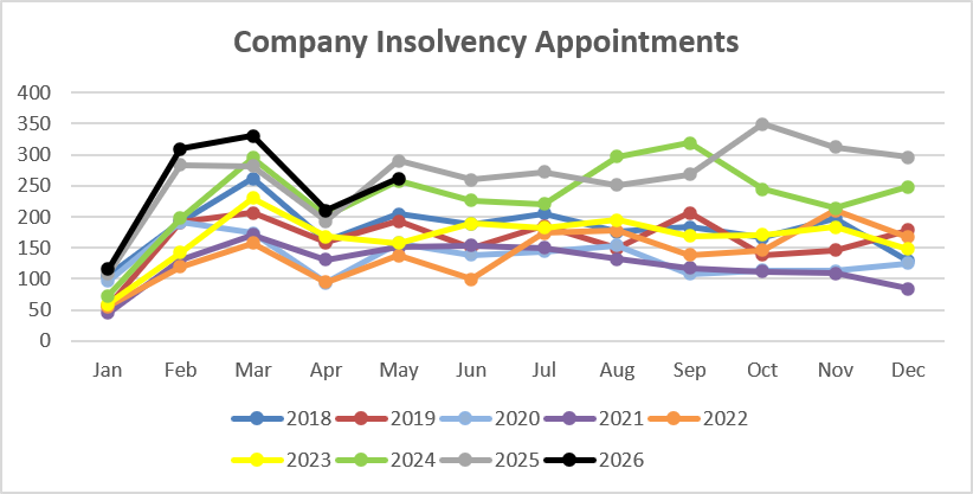

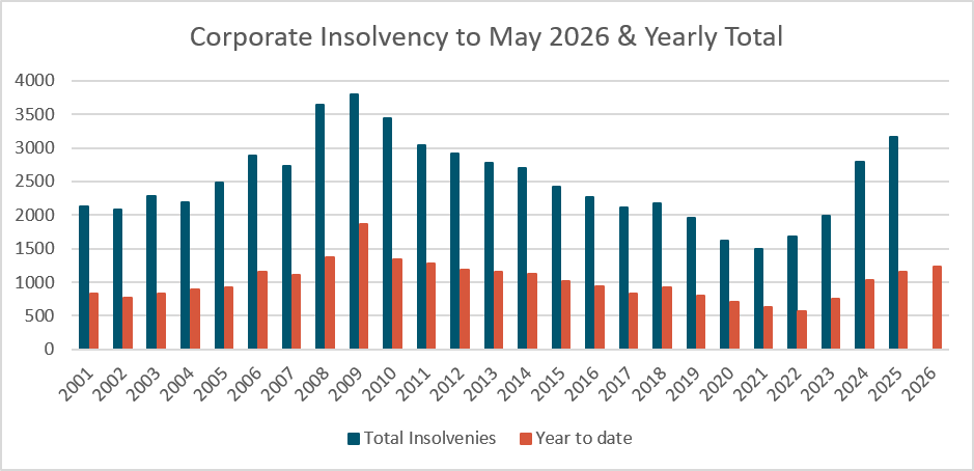

Company Insolvencies – Liquidations, Receiverships, and Voluntary Administrations

May 2026 wasn’t the largest month but continued to post decent figures in line with earlier months.

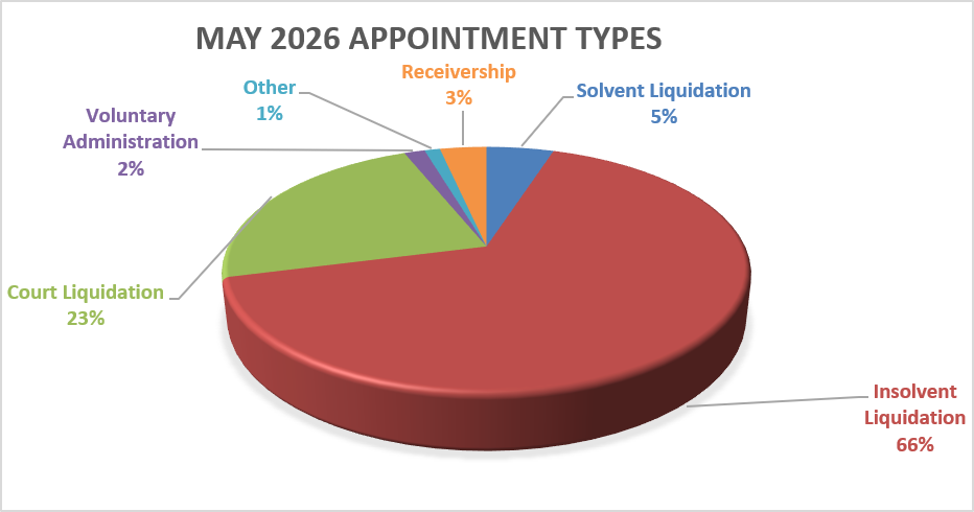

Solvent Liquidations 13

Shareholder Insolvent Liquidations 173

Court Insolvent Liquidations 60

Voluntary Administrations 4

Other 3

Receiverships 9

The above figures were skewed slightly to Shareholder Insolvent Liquidations with the growth in that appointment type coming straight out of Solvent Liquidations. The other appointment types are in line with their long-term averages.

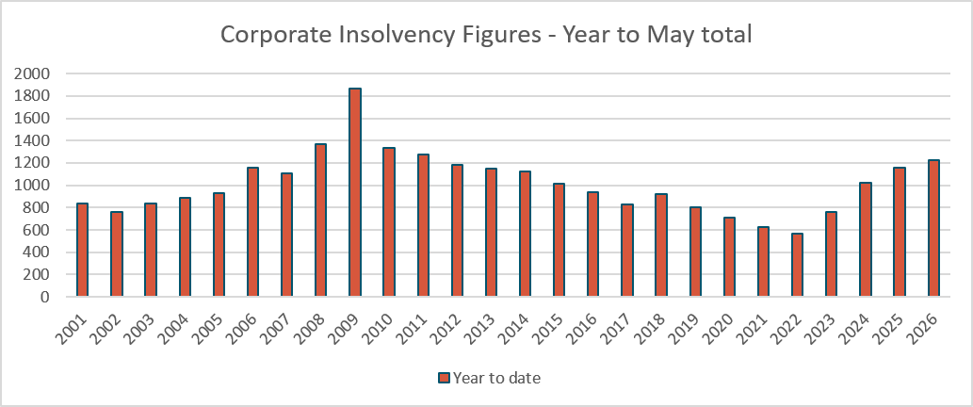

While the month didn’t reach new highs it did keep 2026 above the past few years back to be in line with 2011/2012.

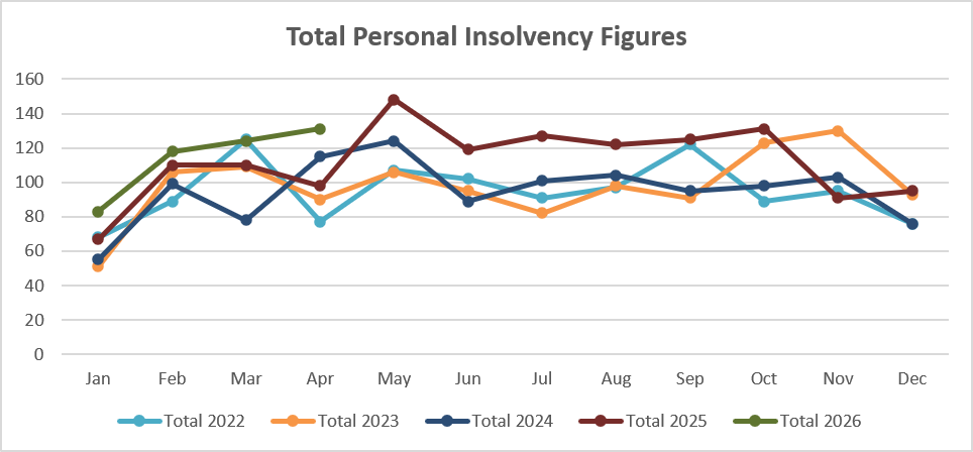

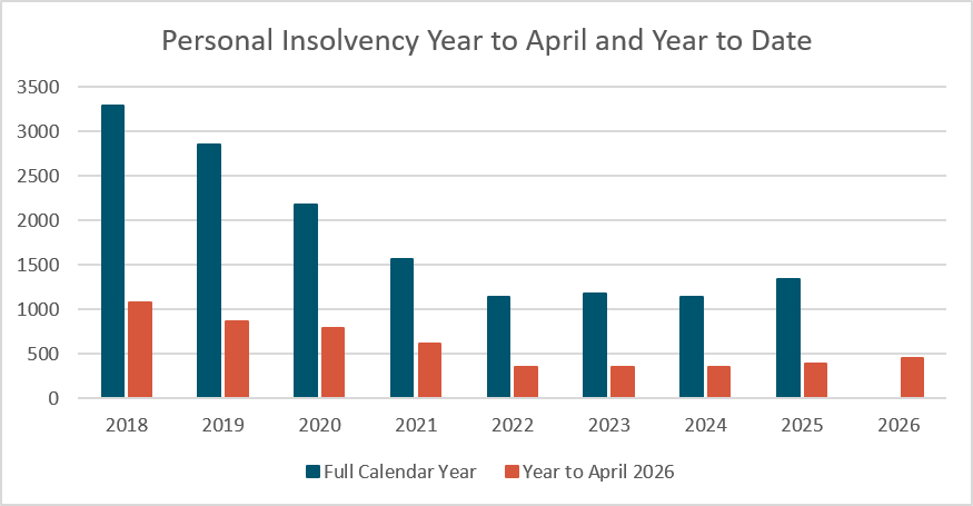

Personal Insolvencies – Bankruptcy, No Asset Procedure and Debt Repayment Orders.

The small gains over the past few months have started to accumulate with a rise now visible for personal insolvency in 2026, it’s by no mean massive compared to pre covid years but if it continues it may eventuate into the long-delayed rise in personal insolvency.

Where to from here?

We continue to track towards a big year as we head into the midpoint for the year. As confirmed in the most recent budget the stresses on the economy are not going away this year at least without dramatic change.

If you want to have a chat about any points raised or an issue you may have you can call on 0800 30 30 34 or email This email address is being protected from spambots. You need JavaScript enabled to view it..

Budget 2026: Insolvency in focus

12 June 2026

Budget 2026 may not have been pitched as insolvency focused, but in practice, that’s exactly what parts of it deliver.

Two changes stand out. First, unpaid shareholder current accounts will now be taxed six months after a company is liquidated or struck off. Second, Inland Revenue is getting a further $15m per annum to sharpen its enforcement capability.

Anyone working in insolvency will recognise the problem immediately.

Overdrawn shareholder current accounts have long been a fixture of SME failure. A business gets into trouble, drawings have accumulated, and the balance sheet shows a receivable from the shareholder that is rarely recoverable in any practical sense. The company fails, the loan sits there, and in many cases nothing further happens. You cannot get blood from a stone. From a tax perspective, it has historically been possible for that economic benefit to escape the system entirely.

The scale is not trivial. Inland Revenue data shows roughly 119,000 companies were owed nearly $29 billion by shareholders as at March 2024. That figure tells its own story, this has never been an edge case, but it is a very real problem.

Budget 2026 changes the outcome in a very direct way. If that loan is still sitting there six months after the company is removed from the register, it is treated as taxable income of the shareholder. No recovery required. No argument about intent. The system simply steps in and taxes the result.

From an insolvency perspective, that is a fundamental shift.

The traditional “it will never be recovered” narrative no longer ends the analysis. It just changes who bears the cost. Previously, the loss often fell on creditors and, indirectly, the tax base. Now, it sits with the shareholder in a very real and unavoidable way.

That will drive behavior and quickly.

Directors and advisers are far less likely to ignore large debit current accounts as pressure builds in a business. Expect to see more attempts to clean up positions before a formal insolvency event, whether through dividends, salaries, or cash repayments where possible.

Layered on top of this is the increase in Inland Revenue funding.

An extra $15m per annum is not about optics, it is about capability. Inland Revenue has been signaling for some time that it sees shareholder loans as an area of concern, particularly where companies are wound up with those balances still outstanding. The current rules, in IRD’s view, have allowed too many situations where tax is deferred and ultimately never collected.

With more resources, that concern will translate into action.

In practical terms, Inland Revenue is likely to be more visible earlier. More queries. More intervention before insolvency. The days of IRD sitting passively letting the debt grow are probably numbered, with a growing debtor book the government of the day is providing them with clear instructions to go collect what is owing.

For those advising directors, the message is simple. Shareholder current accounts can no longer be left to drift and need to be addressed ideally in the year they are being incurred to lessen the impact of having to deal with multiple years at one time. What was once a grey area is becoming black and white.

None of this will reduce insolvency volumes, it will likely cause it to grow with increased enforcement. But it will change how insolvencies play out and who ultimately pays.