Insolvency by the Numbers #62: NZ Insolvency Statistics February 2026

Insolvency by the Numbers #62: NZ Insolvency Statistics February 2026

What have the insolvency numbers done in February 2026, we also look at what could be instore for the rest of the 2026 for personal and corporate insolvency.

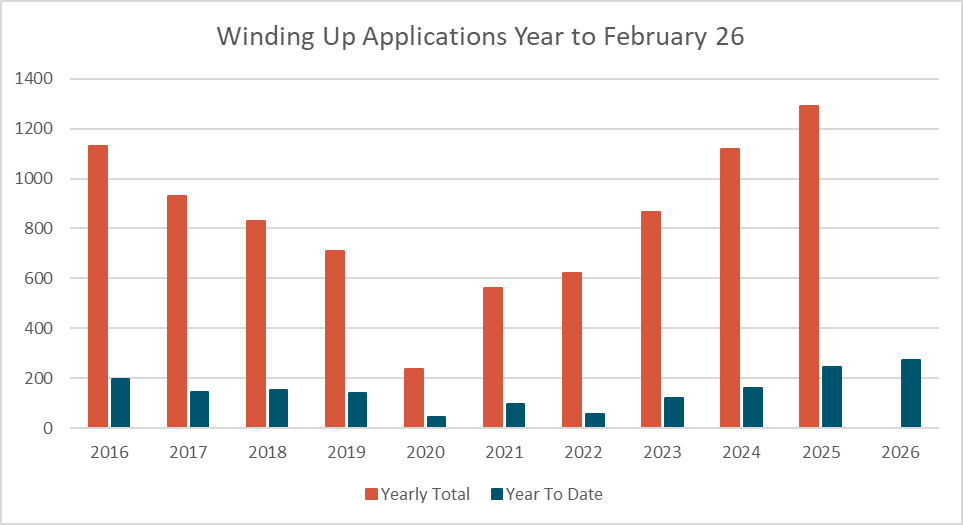

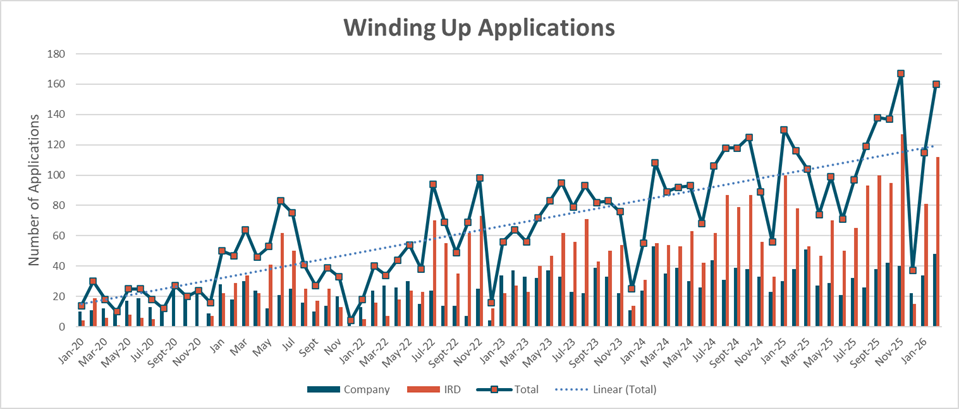

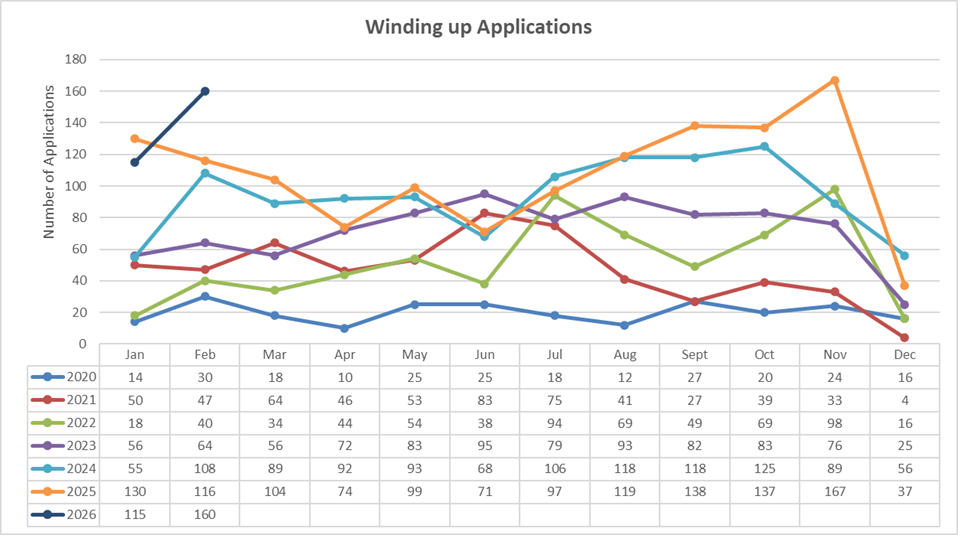

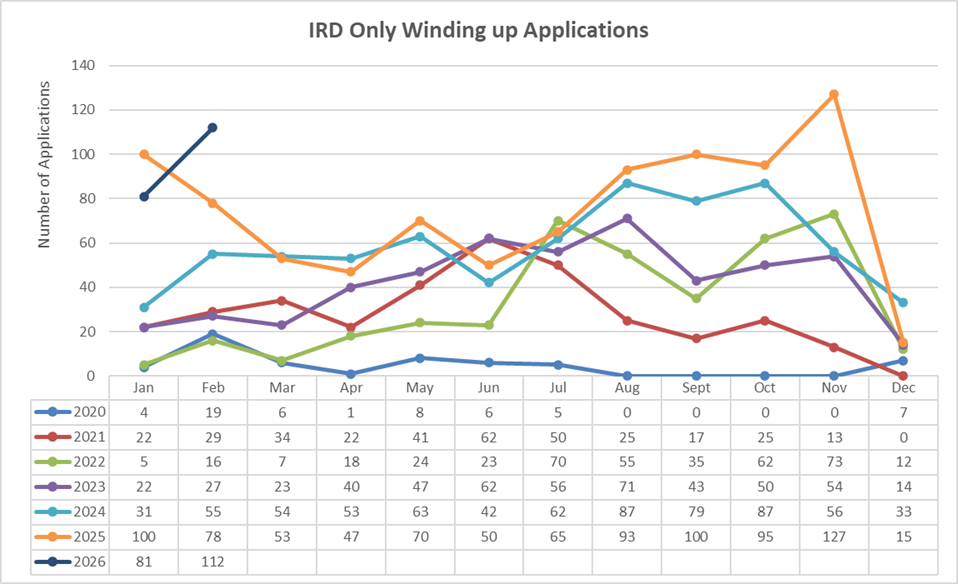

Winding Up Applications

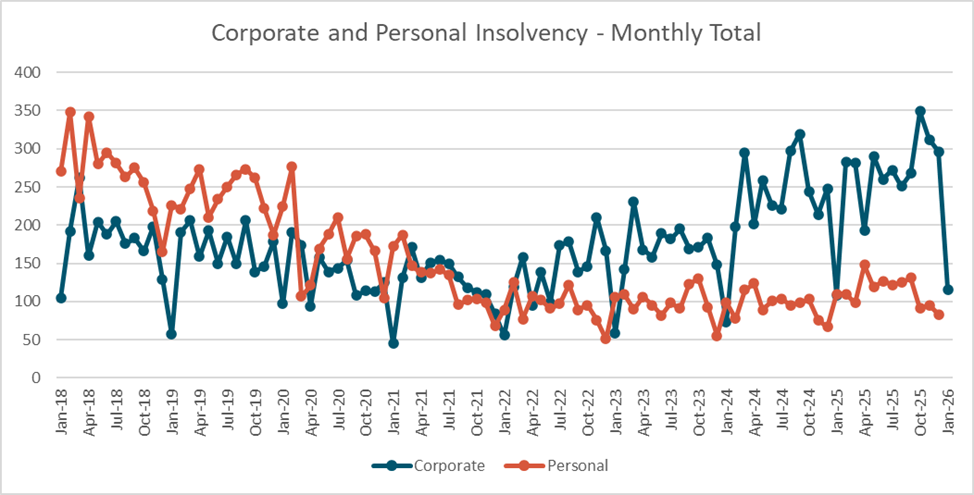

We have started off the year with a bit of pressure seen in the number of winding up applications advertised, it has exceeded what we saw in 2025.

Businesses are still under the pump, and it is being driven by the IRD in large part making up 193 of the 275 January and February winding up applications.

February had 160 applications advertised making up for the slightly slower start seen in January 2026. February 2026 was the 2nd highest month for total appointments over the last 10 years with only the 167 applications seen in November of 2025 exceeding it.

The IRD applications in February made up 112 of the 160, coming in 2nd again only to November 2025 where they advertised 127 appointments in the month.

A big month for winding up applications and it will flow through into a big March and April for appointments through the courts as pressure on delinquent debtors continues to grow.

2026 looks like it will exceed 2024 an off the back of February potentially 2025. However, it is very much still early days to predict this particularly in an election year There remains a lot of pressure in the market with higher than desired inflation, no further drops in the OCR likely, and war likely influencing businesses cost margins as fuel price shocks flow through the supply chain and create additional uncertainty.

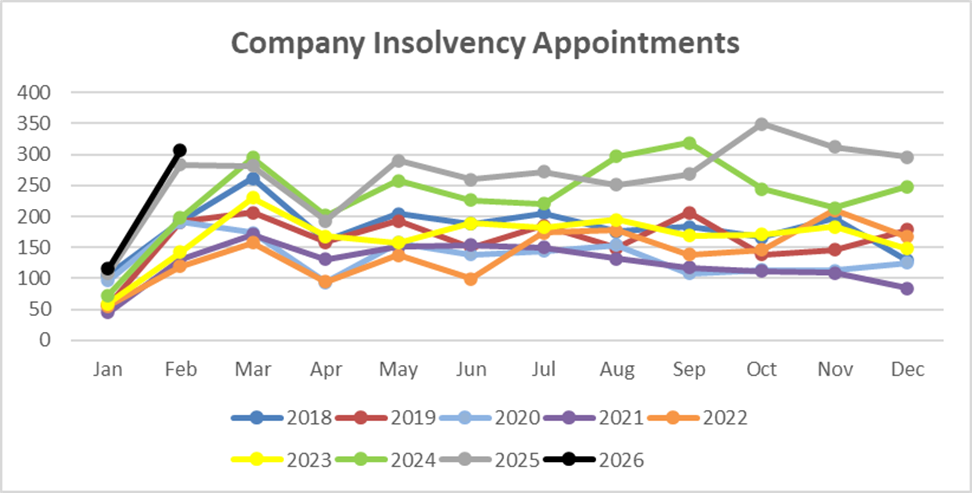

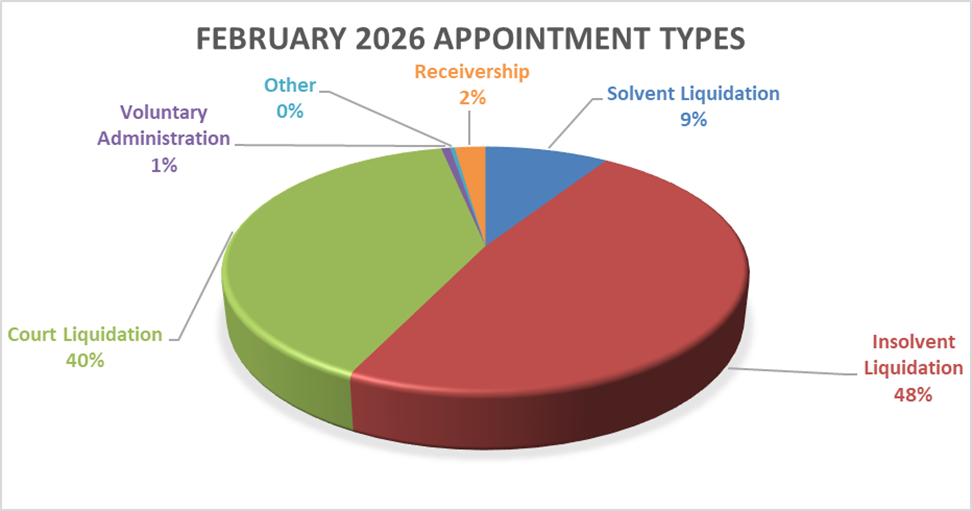

Company Insolvencies – Liquidations, Receiverships, and Voluntary Administrations

February 2026 continued the January trend coming in above the comparative months in 2025 it is looking like LIP’s will be in for another busy year. Appointment figures are still down on the GFC figures but are in line with wat was experienced in the shoulder years of 2010 and 2011.

With another month of high levels of winding up application the number of court appointed liquidations is expected to remain high currently sitting at 40% compared to its long-term share around 27%.

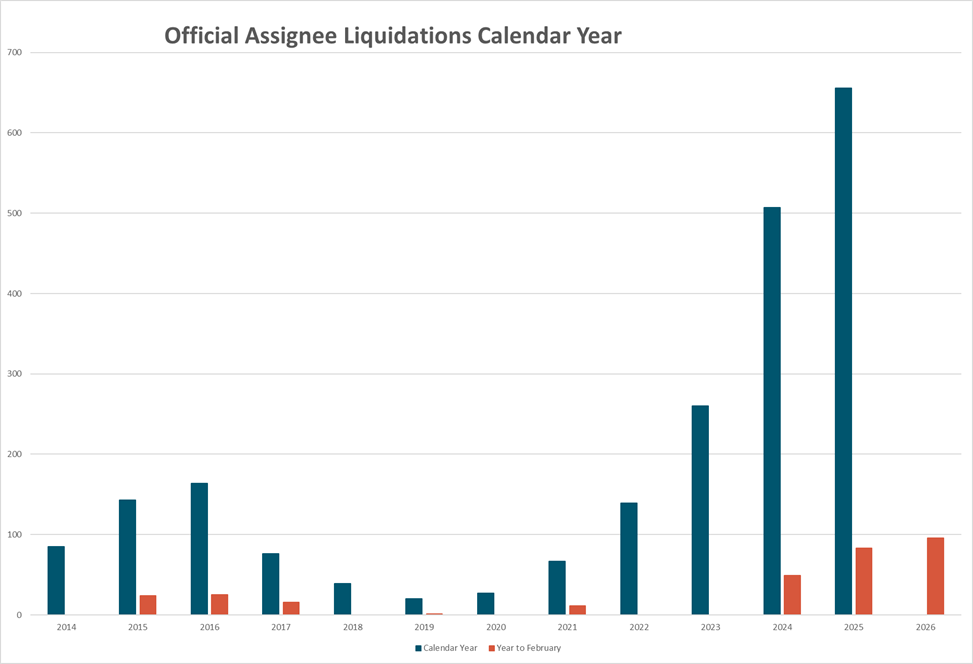

The Official Assignee took 95 liquidation appointments in February, almost all of them were IRD court applications. They continue to be the busiest liquidator in the country taking more in one month than a lot of practitioners take in one year.

Personal Insolvencies – Bankruptcy, No Asset Procedure and Debt Repayment Orders.

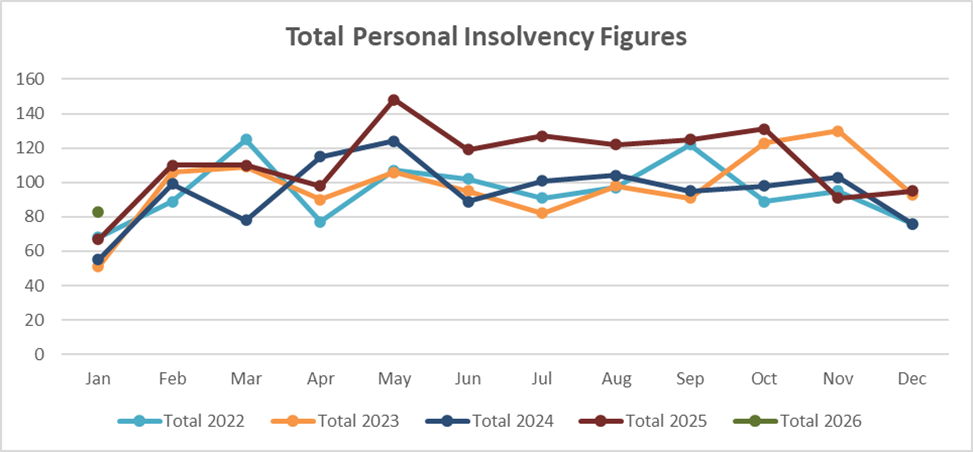

Personal insolvency figures saw a lift in January when compared to the same month in the last few years but it was not a noticeable jump.

Comparatively they took 44 bankruptcies in January but have on average in 2025 taken 55 liquidations per month with highs of 105 in some months.

At this point we continue to expect more of the same for the first half of 2026 as we head into the election.

Where to from here?

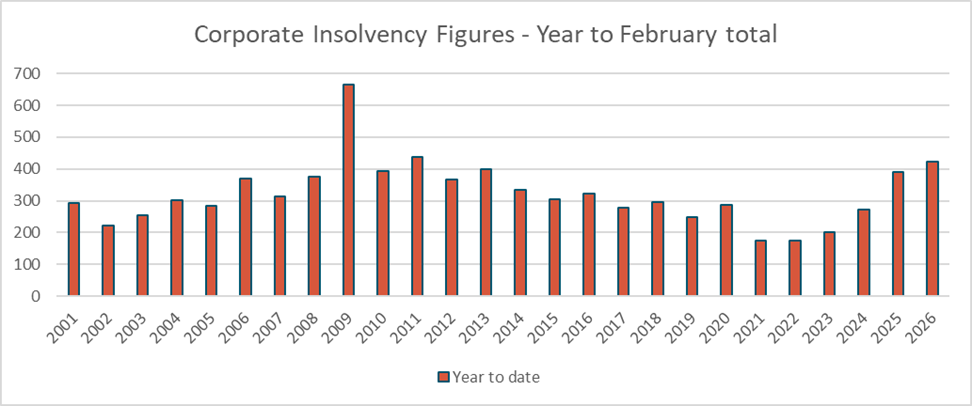

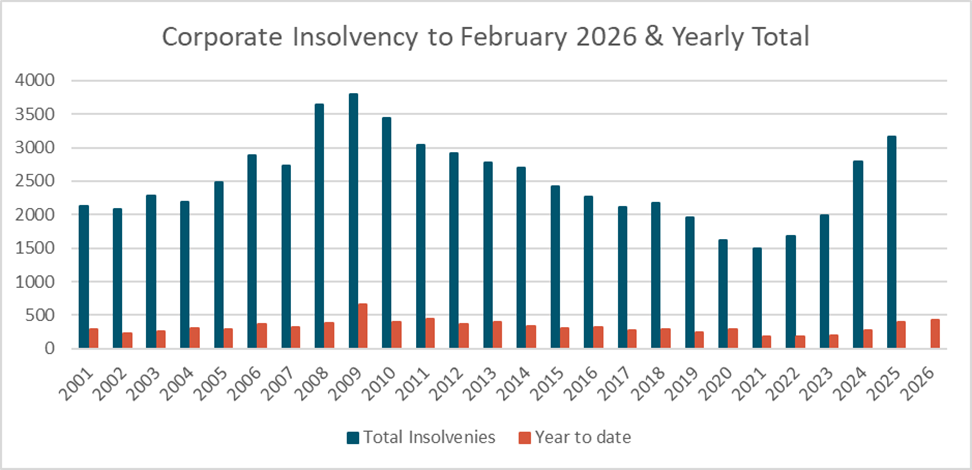

2026 will be an interesting year with an election in the tail end, based on 2024 and 2025 insolvency figures appointments should continue to track up and look to be even higher than what we saw in 2025.

The economy is by no means in the free and clear and has some rough time ahead on the way to recovery. How this plays out with the wait and see approach people take in an election year means the pain may be prolonged and pushed out into 2027.

As always its better to take action and act early, it will often get a better result for all stakeholders.

If you want to have a chat about any points raised or an issue you may have you can call on 0800 30 30 34 or email This email address is being protected from spambots. You need JavaScript enabled to view it..

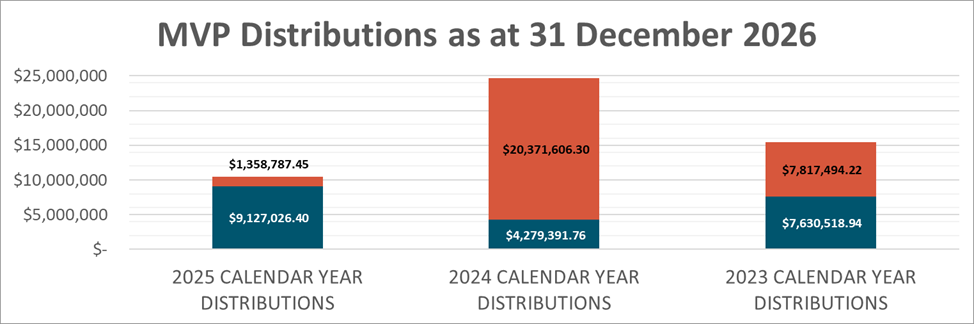

Calendar Year End 2025 McDonald Vague Distributions

1 March 2026

As licensed insolvency practitioners, our principal duty under section 253 of the Companies Act 1993 (copied at end of article) is to take possession of, protect, realise, and distribute assets to creditors in a reasonable and efficient manner. This statutory obligation sits at the core of how McDonald Vague operates and guides our approach on every appointment.

In practice, this means returning funds to the people and organisations who rely on them most employees awaiting wage and holiday pay arrears, small business owners needing overdue funds to stabilise cashflow, and the IRD chasing their tax arrears. Ensuring meaningful distributions is central to our role and a key measure of effective insolvency administration.

Our ability to make distributions at scale stems from our experience in identifying, recovering, and realising assets across a wide range of situations, supported by efficient processes and responsible fee management, a longstanding focus of the firm.

2025 Distribution Summary

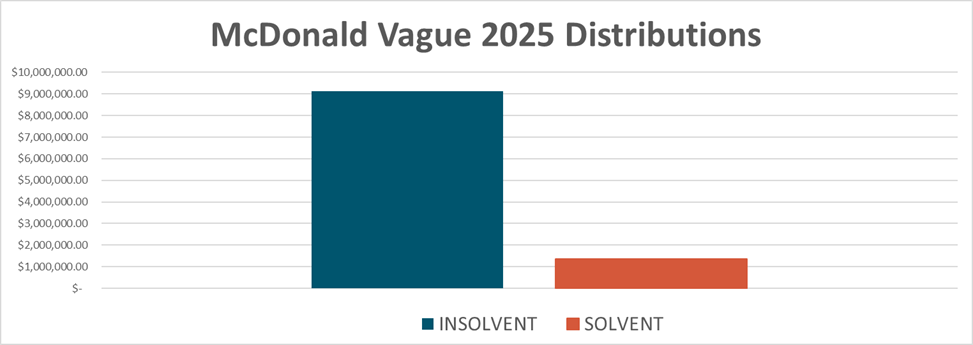

Across all insolvent and solvent appointments concluded within the 2025 calendar year, McDonald Vague paid out a total of:

Insolvent Appointments: $9,127,026.40

Solvent Appointments: $1,358,787.45

These results reflect consistent performance across our portfolio rather than reliance on any single appointment.

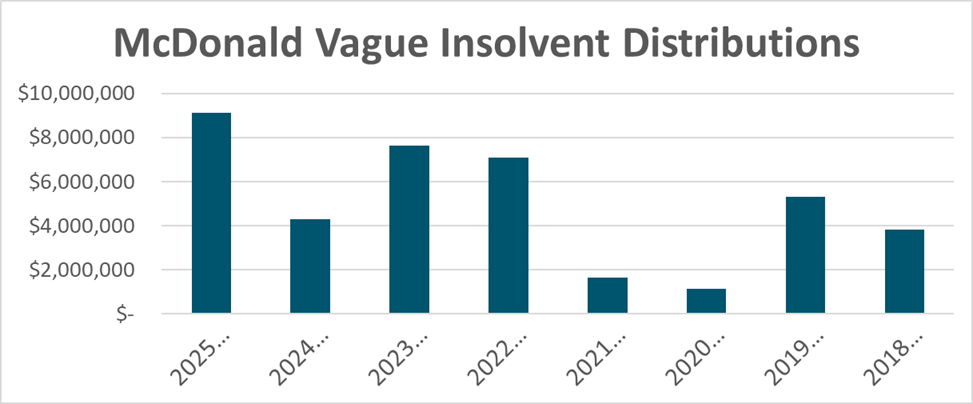

Insolvent Company Distributions

In 2025, a total of $9,127,026.40 was distributed to creditors in insolvent company liquidations. These distributions were made across 56 separate appointments, demonstrating diversification of recoveries and steady throughput of work across the year.

The breakdown of these distributions is as follows:

Preferential Creditors: $547,455.30

Secured Creditors: $6,137,593.50

Unsecured Creditors: $2,441,977.60

Returning funds to unsecured creditors often the group with the least expectation of recovery continues to be a point of pride for our team.

Solvent Liquidation Distributions

Solvent liquidations also formed part of our 2025 workstream, delivering $1,358,787.45 back to shareholders across various appointments.

Solvent liquidations remain an efficient and legally robust mechanism for companies that have completed their purpose and can pay all liabilities within 12 months — a process we regularly support for business owners undertaking restructuring, group simplification, or succession planning.

Our Ongoing Focus

As one of New Zealand’s leading insolvency and business recovery firms, our emphasis remains on:

Maximising creditor returns

Responsible fee management

Efficient realisation and distribution of assets

Clear, practical communication with stakeholders

Each distribution reflects the practical value we deliver to creditors, business owners, and the wider commercial community.

If you would like to discuss any aspect of the 2025 results or require advice on an appointment, our licensed insolvency practitioners are available to help.

Section 253 of the Companies Act 1993 sets out:

“Duties, rights, and powers of liquidators

253 Principal duty of liquidator

Subject to section 254, the principal duty of a liquidator of a company is—

(a) to take possession of, protect, realise, and distribute the assets, or the proceeds of the realisation of the assets, of the company to its creditors in accordance with this Act; and

(b) if there are surplus assets remaining, to distribute them, or the proceeds of the realisation of the surplus assets, in accordance with section 313(4)—

in a reasonable and efficient manner.” – emphasis added

A Lesser Known Section of the Tax Act

1 March 2026

In situations where PAYE has been deducted from wages but not paid to Inland Revenue, directors and associated persons of close companies may face unexpected personal tax consequences. Inland Revenue has the ability under Section LB 1(3) of the Income Tax Act 2007 to reassess an individual’s tax return and limit their PAYE tax credits to the amount actually received by the Commissioner. Given the number of liquidations we manage where PAYE arrears are present, it is important that directors understand this rule. The article below explains how the section operates and why Inland Revenue may invoke it.

Section LB 1(3) — Income Tax Act 2007

We want to take this opportunity to draw your attention to a lesser‑known or used section of the Income Tax Act 2007 (ITA 2007) that we have seen applied by the Inland Revenue (IRD) in some recent liquidations. The section, however, can be used in other situations when PAYE has not been paid to the IRD by an employer.

We think it is important that directors and advisors are aware of this section where directors and/or associated persons are being paid on the payroll of a close company(1) (all or part of their remuneration) and having PAYE deducted, that when the employer does not pay (or is contemplating not paying) the PAYE to the IRD.

Section LB 1(2) of the ITA 2007 allows a tax credit for the tax year equal to the amount of tax withheld from a PAYE income payment of a person who is an employee.

Section LB 1(3) of the ITA 2007 limits this credit to the amount of tax paid by the employer to the Inland Revenue if certain conditions are met.

This section allows the IRD to reassess the income tax return of a director or shareholder if the amount of the tax credit is more than the amount of tax paid to the Commissioner if

(a) the employer is a close company(1); and

(b) the employer and the person are associated persons, or the employer and the spouse, civil union partner, or de facto partner of the person are associated persons; and

(c) the employer withheld the amount of tax for the PAYE income payment shown in their employment income information.

In a liquidation, this section is not something the Liquidator has any control over as it impacts the individual taxpayer and relates to events before the Liquidation. This is a section the IRD can apply at its discretion to the individual taxpayer.

A Simple Example

A is a director/employee who has been paid $150,000 during a tax year and $42,414 tax had been reported as PAYE deducted at source through Payday filing.

The company still owes $20,000 of this amount in unpaid PAYE.

The IRD can reassess A’s tax return to reflect only the $20,000 having been paid against their earnings, making them personally liable for the shortfall in tax due.

While Section LB 1(3) is technical in nature, its impact can be significant for directors and associated persons when PAYE has been withheld but not paid. Importantly, this is a matter that Inland Revenue deals with directly with the taxpayer and sits outside the liquidator’s control. Directors and advisors should therefore be mindful of PAYE arrears as they arise, as the consequences can extend beyond the company and into an individual’s personal tax obligations.

Definition

(1) Close company:

A company that has five or fewer natural persons (associated persons counted as one) who either hold voting interests, or hold market value interests in the company of more than 50%.

Reference

Section LB1 of the Income Tax Act 2007 can be found at:

https://www.legislation.govt.nz/act/public/2007/0097/latest/DLM1517915.html