Insolvency by the Numbers #64: NZ Insolvency Statistics April 2026

11 May 2026

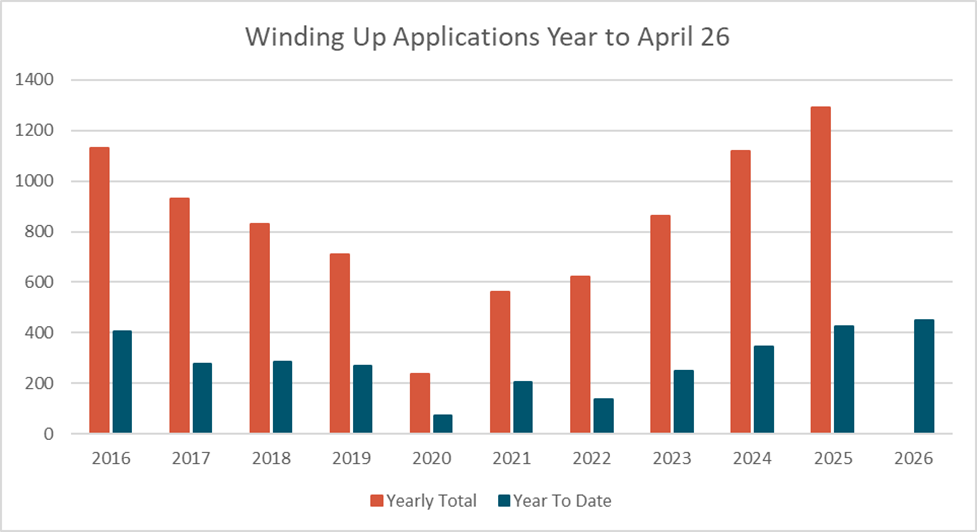

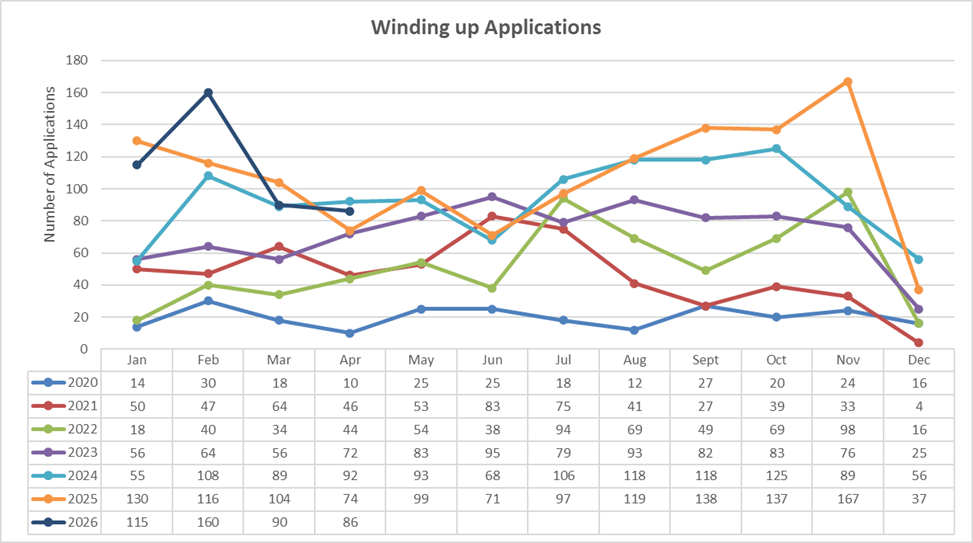

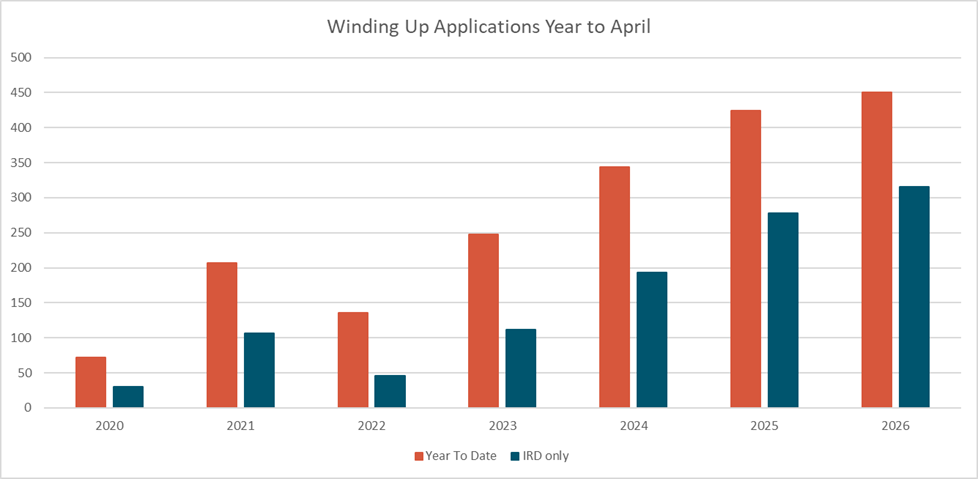

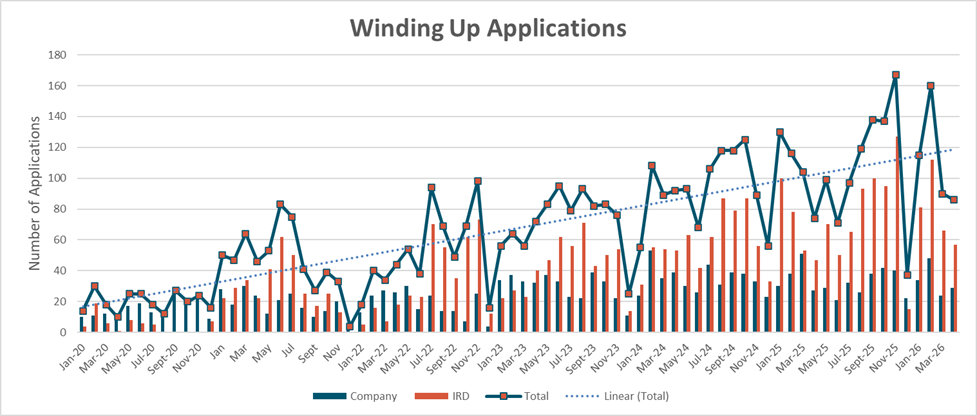

Winding Up Applications

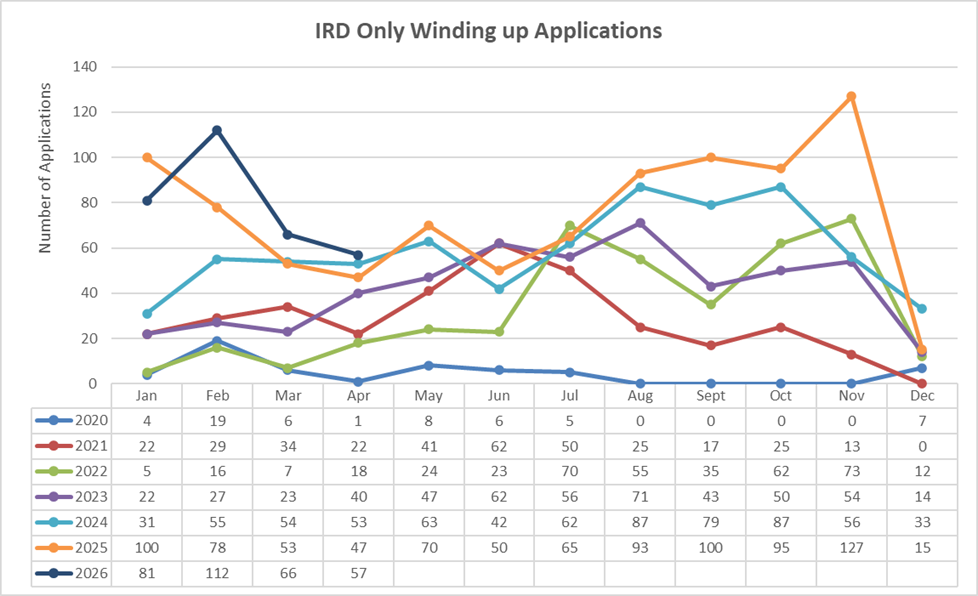

April 2026 NZ Liquidation Winding Up Applications keep the ball rolling on the continued highs of the last 10 years with the largest 4 months to start to year.

Of note the applications for the month were slightly behind 2024's figures for April, this was driven in 2024 by a bumper month for non IRD creditors chasing debtors. IRD however have continue their above past years enforcement levels and have yet to slow up.

At this stage in the year historically Winding Up Applications have levelled out somewhat till they once again jump in July to peak in November. We remain on track to beat out 2025 for total applications for the year. We will continue to see more and more court appointed liquidations increasing their share of the total insolvencies.

We expect that by June this year there will be more winding up applications in 6 months than what we saw in the 2021 and 2022 years.

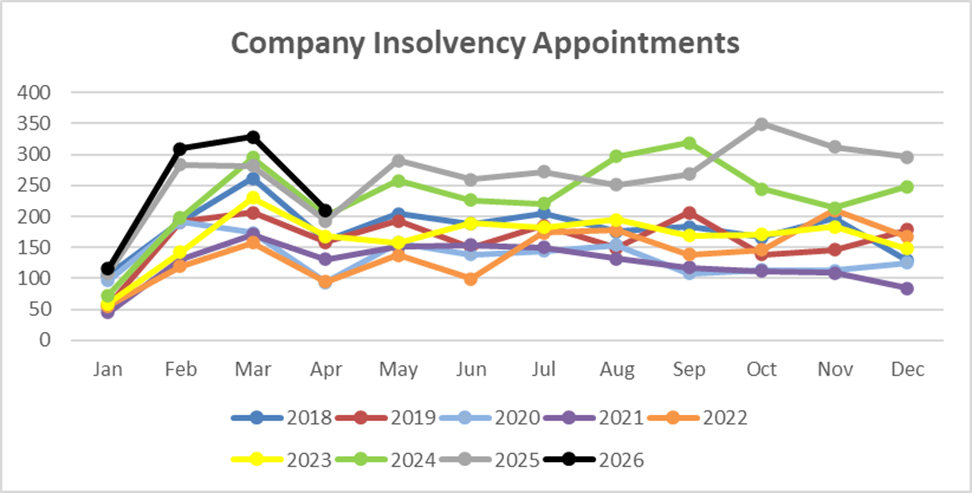

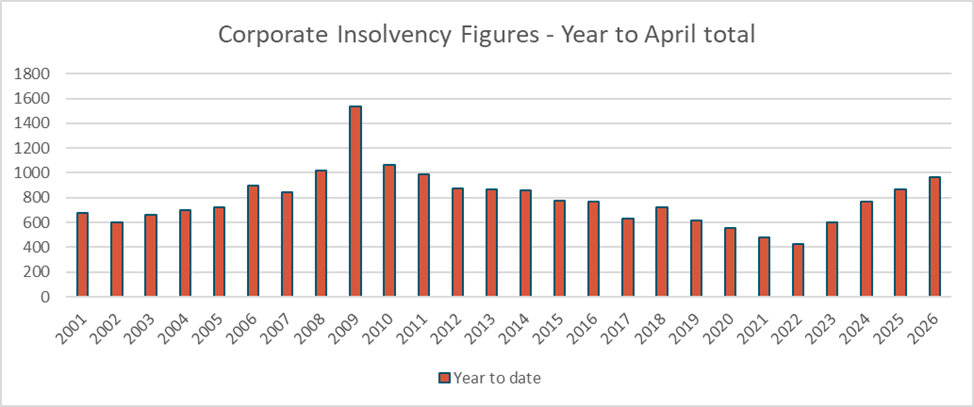

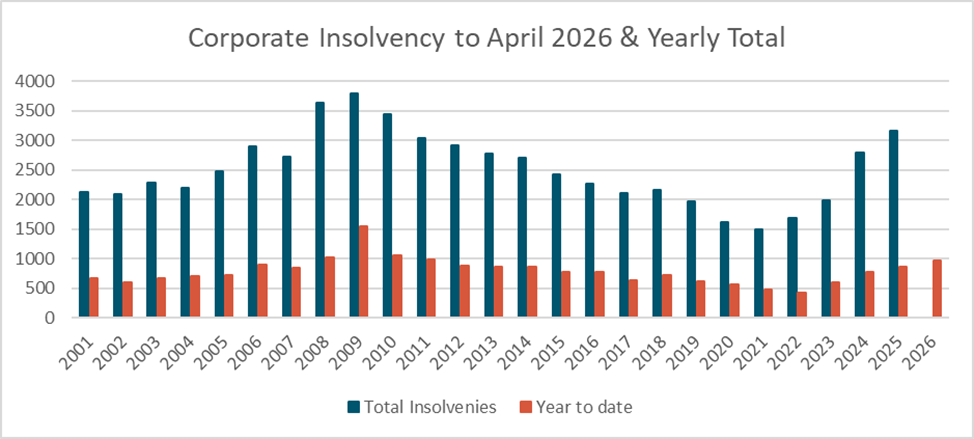

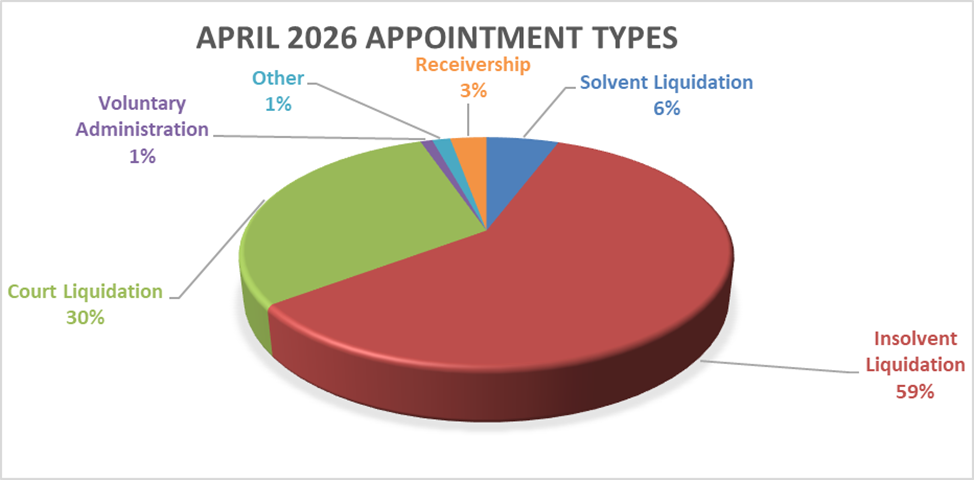

Company Insolvencies – Liquidations, Receiverships, and Voluntary Administrations

Another month and another high for the last 15 years. While not up to the levels seen during the GFC, emphasising that this downturn is longer rather than short and sharp, we continue to bump up against the shoulder year (2008 & 2011) appointment figures.

Solvent liquidations remain below their long-term average of 11% overall, as there appear to be less cashed up companies looking to wind up. Insolvent shareholder liquidations and court liquidations both remain above their long-term shares of the total appointments taking up the lost solvent share.

With another month of elevated levels of Winding Up Applications the number of court liquidations is expected to remain high.

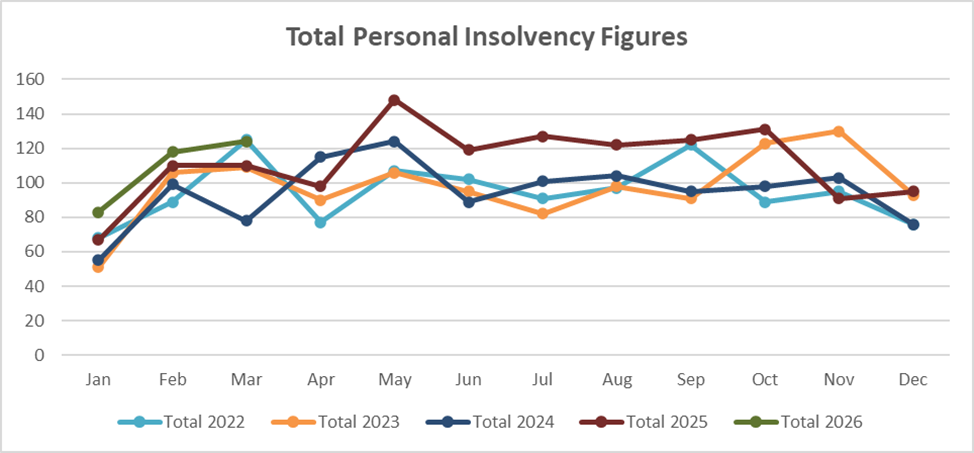

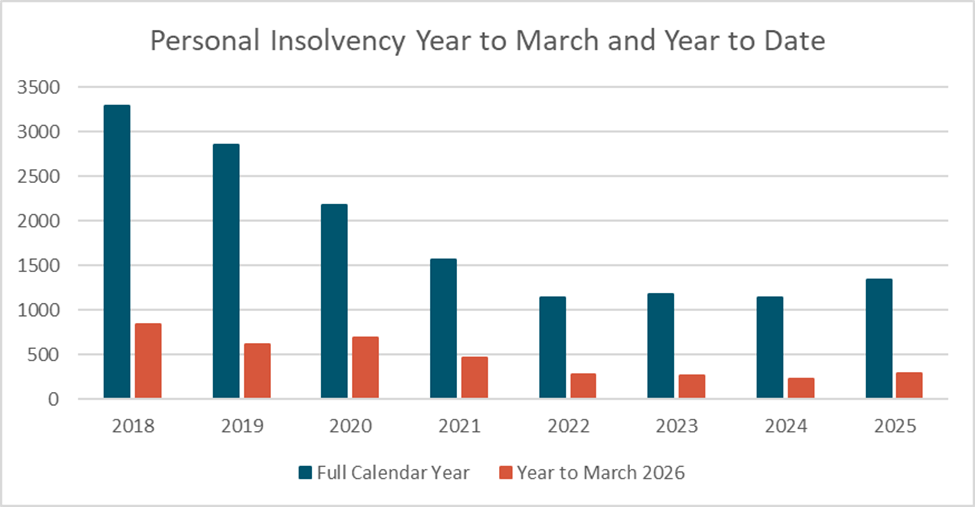

Personal Insolvencies – Bankruptcy, No Asset Procedure and Debt Repayment Orders.

March saw more of the same on the personal insolvency front with little change. At this point we continue to expect more of the same with only minor rises and drops.

Where to from here?

After a big first third 2026 looks to be another big year unless something drastically changes. The stresses on the economy are not going away.

If you want to have a chat about any points raised or an issue you may have you can call on 0800 30 30 34 or email This email address is being protected from spambots. You need JavaScript enabled to view it..

The “10 Working Day Rule” Following Service of a Winding Up Application

11 May 2026

In New Zealand there is a critical window following the service of a winding up (“liquidation”) application on a company’s registered office. Practitioners commonly refer to this as the “10 working day rule” a practical and strategic timeframe that can significantly affect a company’s ability to control who is appointed as its liquidator.

This article explains the rule, its legal foundation, and its implications in practice.

Overview of the Rule

Once a winding up application is served on a company, the company has 10 working days in which it can still appoint its preferred liquidator (typically via shareholder resolution) without needing the consent of the applicant creditor.

After the 10 working day period expires:

- The company loses its unilateral ability to appoint a liquidator of its choosing.

- Any voluntary appointment requires the consent of the applicant creditor

Why the 10 Working Day Period Matters

Preservation of Shareholder Control

During this initial 10 working day window the company’s shareholders retain full control over the appointment of a liquidator. They can act quickly to appoint a practitioner of their choosing.

Shift in Control After 10 Working Days

Once the period expires the creditor who filed the winding up application gains procedural leverage. A voluntary liquidation initiated by the company is dependent on the creditor agreement. At this stage creditors may prefer their own nominee liquidator they have lined up rather than the one selected by the shareholders. The creditor may agree to the shareholders liquidator in situations where the practitioner is known to them or they did not have one lined up, it will allow for the company to be placed into liquidation earlier that having to wait for the court date and may reduce costs.

If a liquidator is subsequently appointed without the consent of the creditor they will be removed from the appointment and deemed to be invalidly appointed.

Practical Implications for Directors and Advisors

Urgency of Decision-Making

The 10 working day period is strategically critical. Directors must:

- Obtain insolvency advice quickly once served, ideally before this

- Assess solvency and alternatives (e.g. restructuring vs liquidation)

- Decide whether to appoint a liquidator voluntarily

Delay can result in:

- Loss of control

- Increased creditor involvement

- More complex and potentially adversarial proceedings

Tactical Considerations

Appointing a liquidator within the 10 working day window may:

- Avoid Court costs associated with the application

- Allow the company to nominate an experienced or preferred practitioner

- Demonstrate cooperation with creditors

Conversely, failing to act within the timeframe may:

- Lead to a creditor-driven liquidation

- Reduce flexibility in managing creditor relationships

Role of the Applicant Creditor

After the 10 working day period:

- The applicant creditor’s influence increases materially

- They may insist on their nominated liquidator

- A late voluntary appointment will be deemed invalid

This shifts the dynamics from company-led to creditor-driven decision-making.

Summary

The “10 working day rule” is a crucial feature of New Zealand insolvency practice:

- It begins upon service of a winding up application

- It provides a limited window for the company to appoint its preferred liquidator

- After expiry, control shifts toward the applicant creditor and the Court

For directors and advisors, the key takeaway is simple:

Act quickly within the 10 working day window if you want to retain influence over the liquidation process.

Storm Signals: When a Tough Trading Environment Turns Into Insolvency Risk

11 May 2026

Over the past 12-18 months, many New Zealand businesses have been navigating what can best be described as a “slow squeeze.” It hasn’t been a single catastrophic event, but rather a steady accumulation of pressures, these include rising interest rates, increased input costs, tighter consumer spending, and delayed payments.

For professional advisers working closely with clients, the challenge is recognising when normal trading stress crosses the line into genuine insolvency risk and knowing what to do next.

From Pressure to Distress: The Warning Signs

In our experience, business failure is rarely sudden. Instead, it follows a familiar pattern. Early recognition is key to preserving options and protecting outcomes.

Some of the more common early indicators include:

- Persistent cash flow shortages despite profitable trading on paper

- Increasing reliance on creditor stretching (especially IRD or trade creditors)

- Inability to meet tax obligations as they fall due

- Use of short-term funding (overdraft, credit cards, online loans) to cover structural deficits

- Mounting aged receivables with little prospect of recovery

At this stage, many business owners remain optimistic and focused on “turning things around.” The classic she’ll be right attitude NZers are known for. While that mindset is understandable, delay can materially worsen the position for all stakeholders.

The Critical Shift: Directors’ Duties Come Into Focus

Once a company is, or is likely to become, insolvent, directors’ obligations shift. The focus moves away from shareholders and toward creditors.

Continuing to trade while incurring debts that the company cannot realistically repay can expose directors to personal liability. This is an area that has seen increasing attention in New Zealand courts, and it’s something advisers should be proactively discussing with their clients.

It’s not about forcing a business to stop trading prematurely it’s about ensuring decisions are made with clear awareness of the financial position and associated risks and documented correctly.

Why Early Advice Leads to Better Outcomes

One of the biggest misconceptions is that engaging an insolvency practitioner means “the end of the road.” In reality, early engagement often creates more options, not fewer.

Depending on the circumstances, those options might include:

- Informal restructuring: Working with creditors to realign payment terms

- Refinancing or capital injection strategies

- Orderly wind-downs that preserve value and minimise losses

- Formal insolvency processes such as voluntary administration or liquidation, where appropriate

The earlier these conversations happen, the more control directors and advisers retain over the process, they may then plan and the better the likely outcome for creditors.

The Role of Trusted Advisers

Accountants and lawyers are often the first to see the signs. You’re in the numbers, the agreements, and the day-to-day reality of your clients’ businesses.

This places you in a powerful position but also creates a challenge. Raising insolvency concerns can feel uncomfortable, particularly when long-standing relationships are involved.

However, experience shows that clients are generally grateful for early, pragmatic guidance, even when the message is difficult. Framing the conversation around preserving value and protecting stakeholders can help shift the perception from “failure” to “management.”

Common Pitfalls to Avoid

When businesses get into trouble, we frequently see a few recurring mistakes:

- Waiting too long: Hoping trading conditions will improve often leads to a worse outcome

- Selective creditor payments: Prioritising some creditors over others without a clear strategy can create legal risk

- Poor record-keeping: Inadequate financial information makes it harder to assess options and defend decisions

- Avoiding communication: Silence with creditors tends to escalate issues rather than resolve them

Avoiding these pitfalls can significantly improve the position for all involved.

Final Thoughts

Tough trading environments are a normal part of the economic cycle, but the current conditions are testing many businesses that might previously have been considered stable or have never been through a downturn before.

For advisers, the opportunity lies in helping clients act early, make informed decisions, and avoid the compounding effects of delay.

If nothing else, the key message is simple: when it comes to financial distress, time is not neutral. Acting sooner almost always leads to a better outcome.