11 May 2026

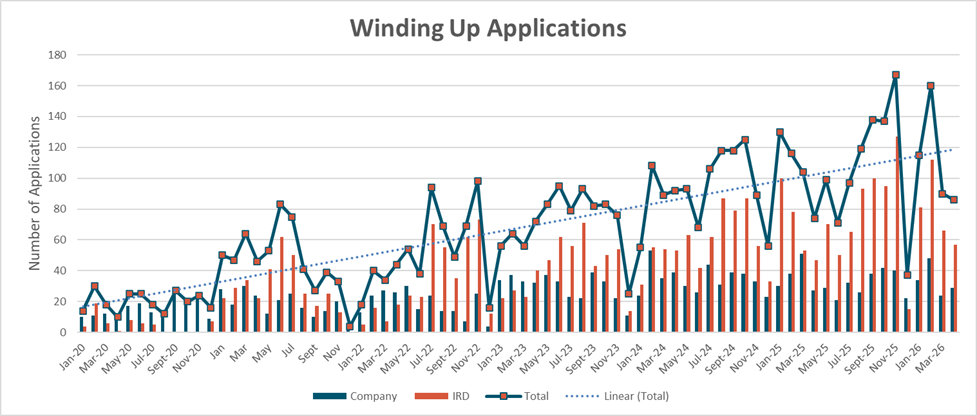

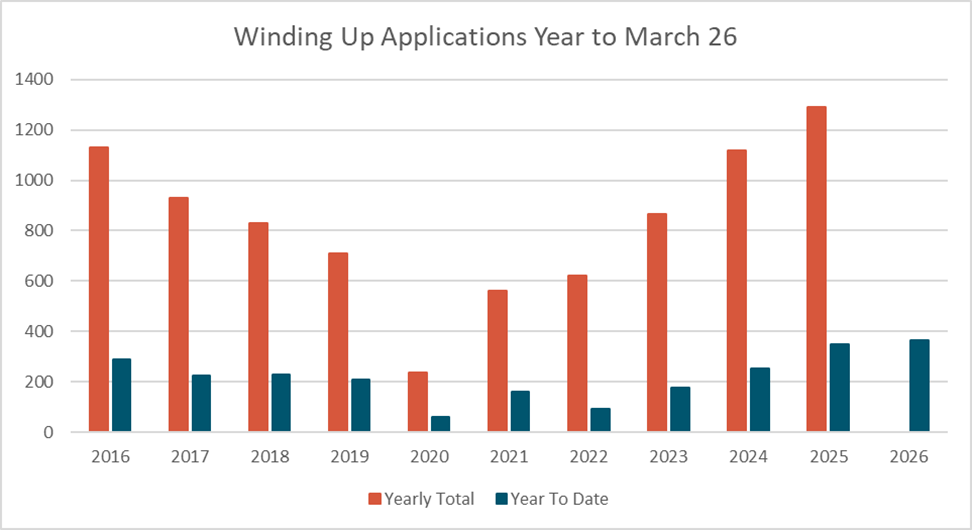

Winding Up Applications

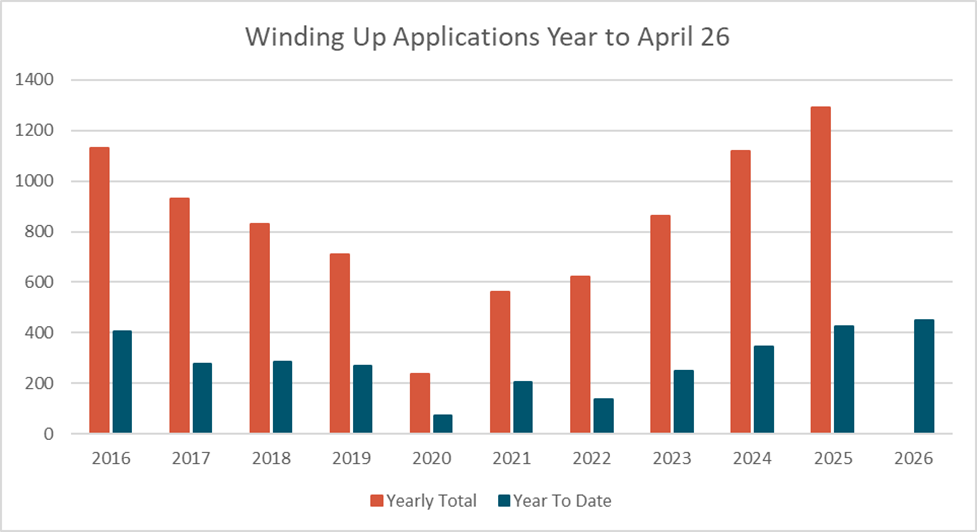

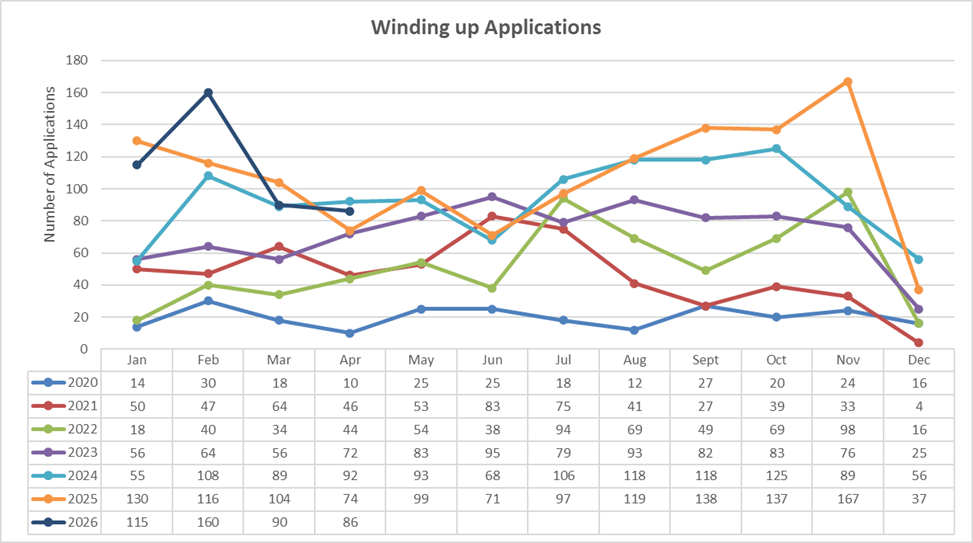

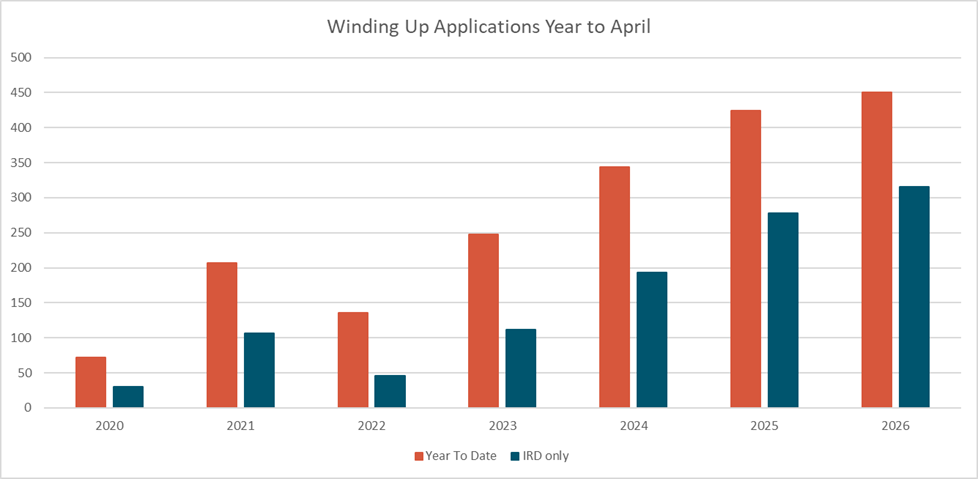

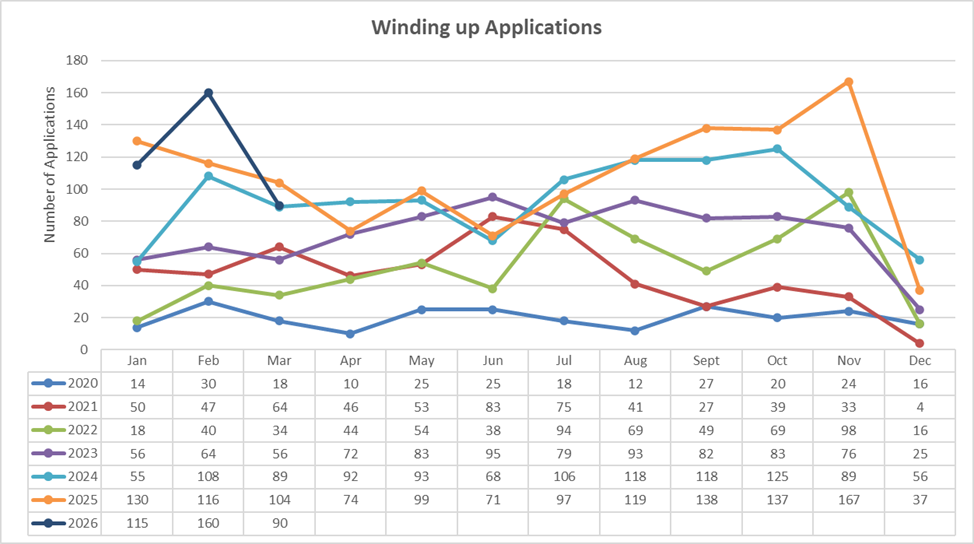

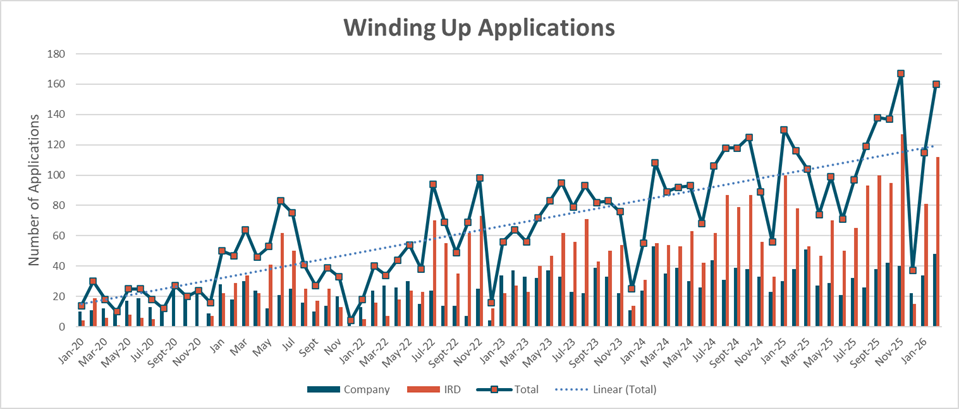

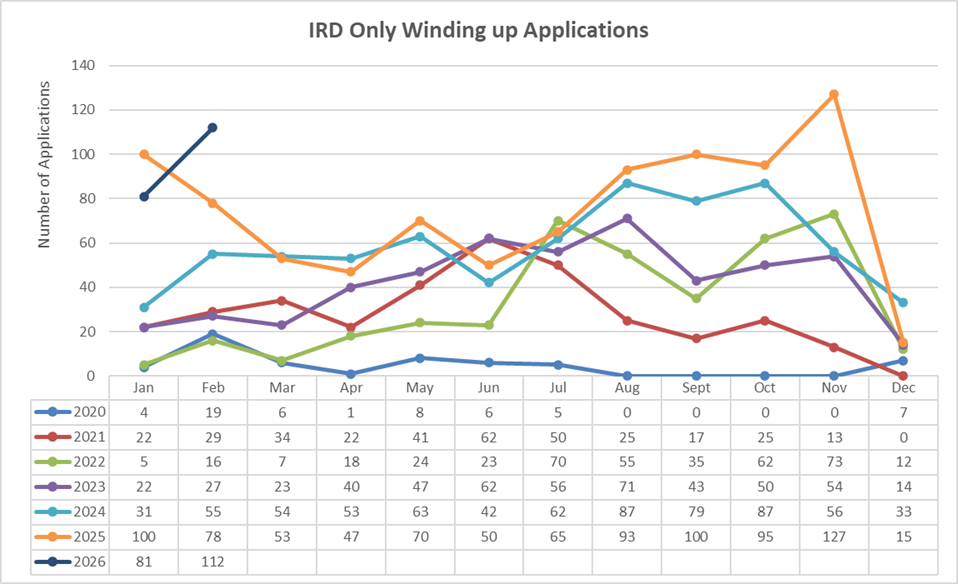

April 2026 NZ Liquidation Winding Up Applications keep the ball rolling on the continued highs of the last 10 years with the largest 4 months to start to year.

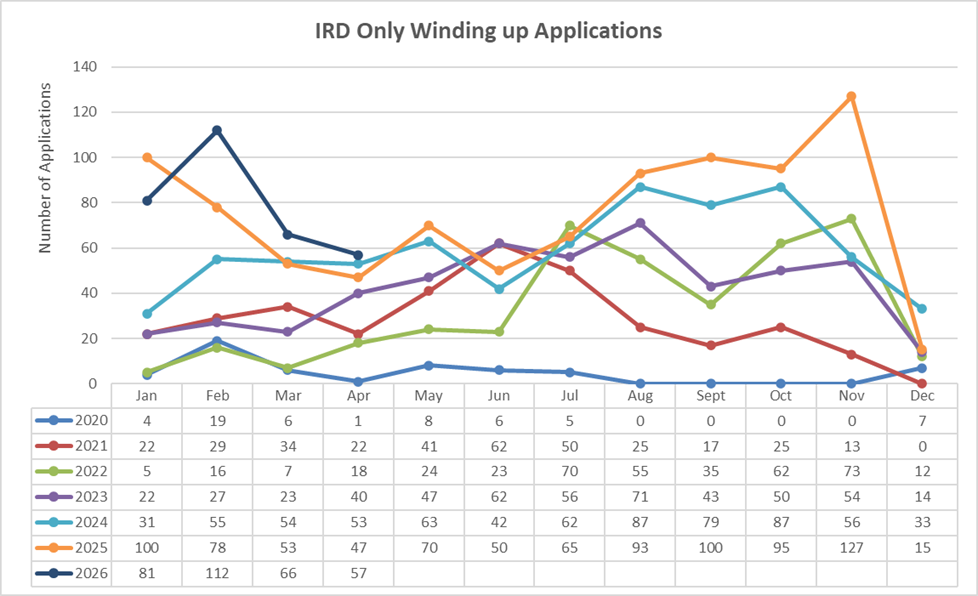

Of note the applications for the month were slightly behind 2024's figures for April, this was driven in 2024 by a bumper month for non IRD creditors chasing debtors. IRD however have continue their above past years enforcement levels and have yet to slow up.

At this stage in the year historically Winding Up Applications have levelled out somewhat till they once again jump in July to peak in November. We remain on track to beat out 2025 for total applications for the year. We will continue to see more and more court appointed liquidations increasing their share of the total insolvencies.

We expect that by June this year there will be more winding up applications in 6 months than what we saw in the 2021 and 2022 years.

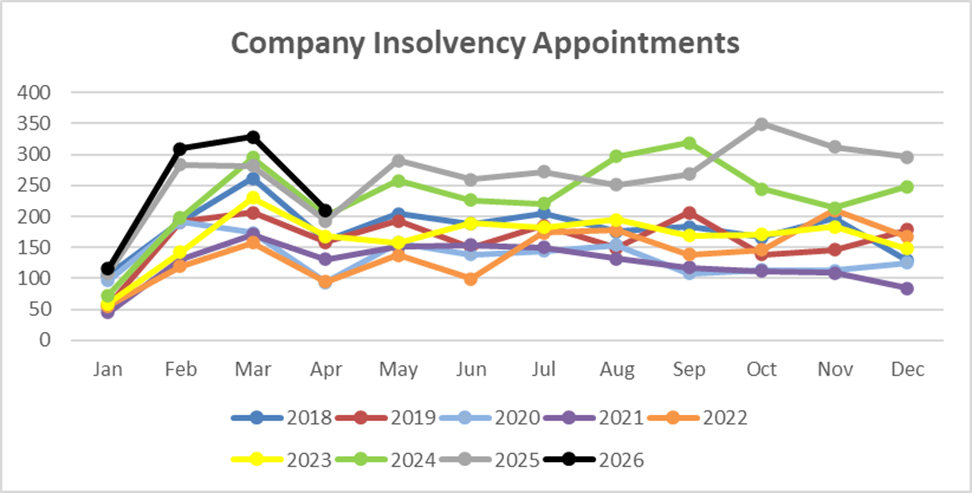

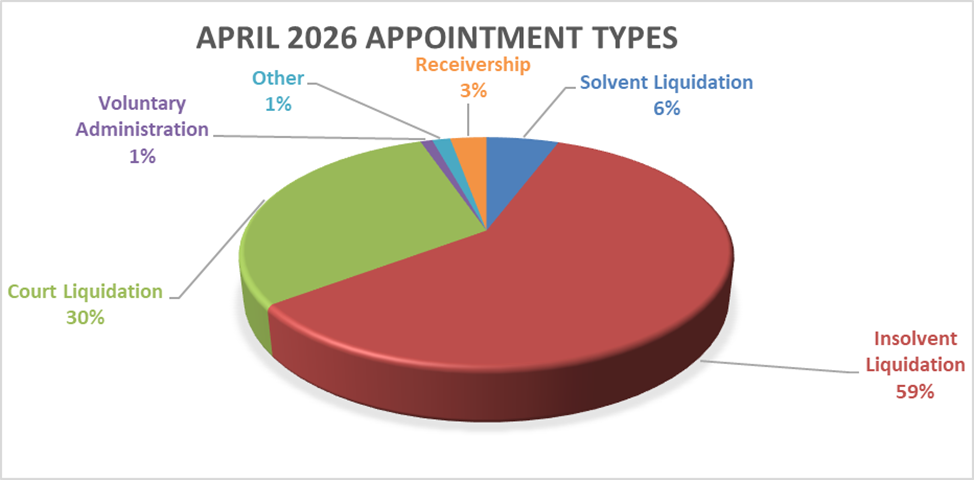

Company Insolvencies – Liquidations, Receiverships, and Voluntary Administrations

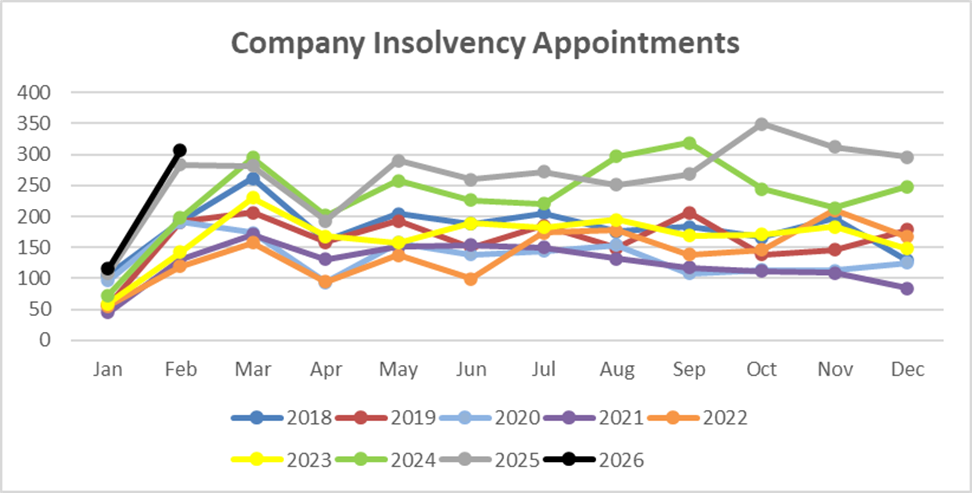

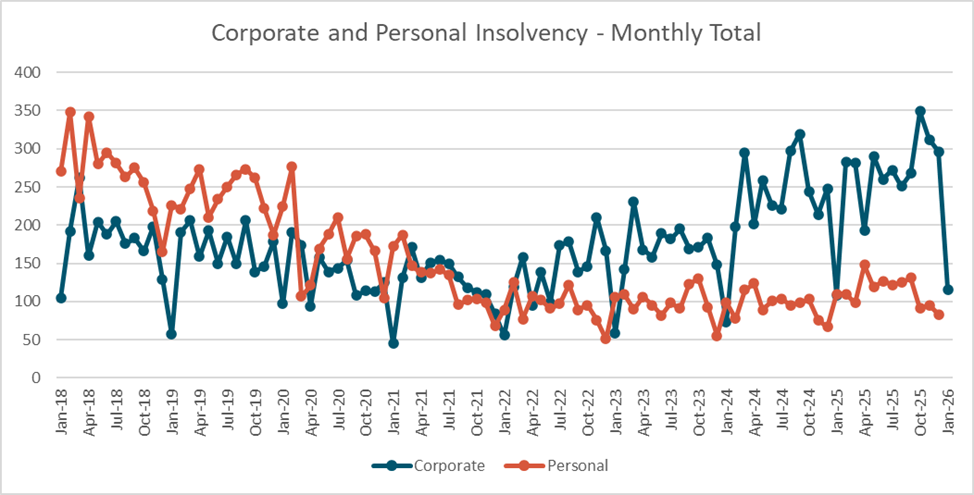

Another month and another high for the last 15 years. While not up to the levels seen during the GFC, emphasising that this downturn is longer rather than short and sharp, we continue to bump up against the shoulder year (2008 & 2011) appointment figures.

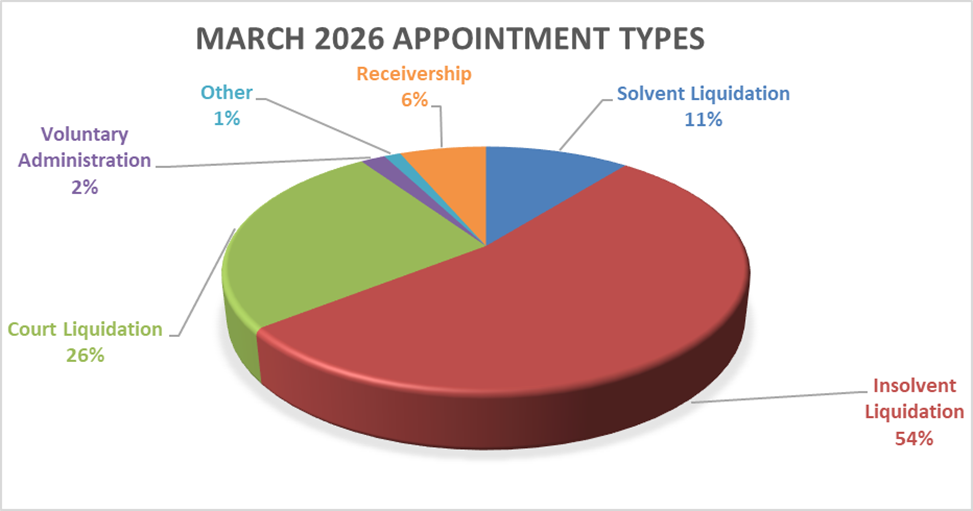

Solvent liquidations remain below their long-term average of 11% overall, as there appear to be less cashed up companies looking to wind up. Insolvent shareholder liquidations and court liquidations both remain above their long-term shares of the total appointments taking up the lost solvent share.

With another month of elevated levels of Winding Up Applications the number of court liquidations is expected to remain high.

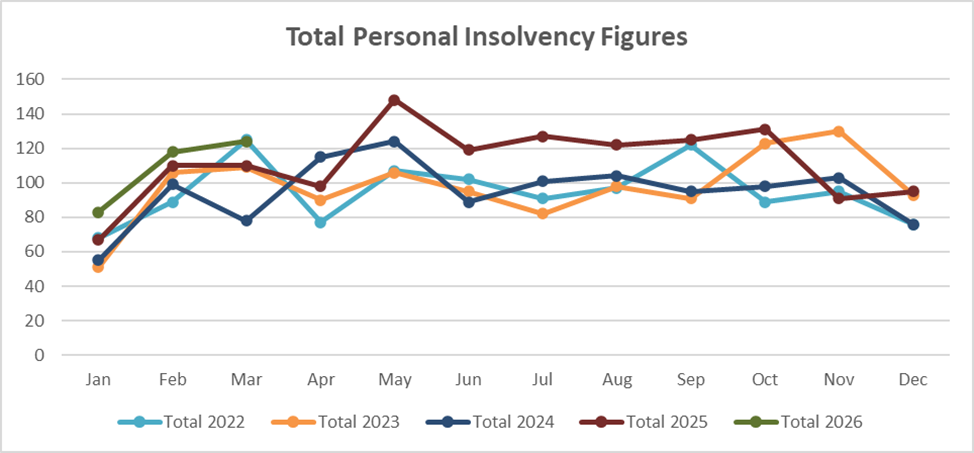

Personal Insolvencies – Bankruptcy, No Asset Procedure and Debt Repayment Orders.

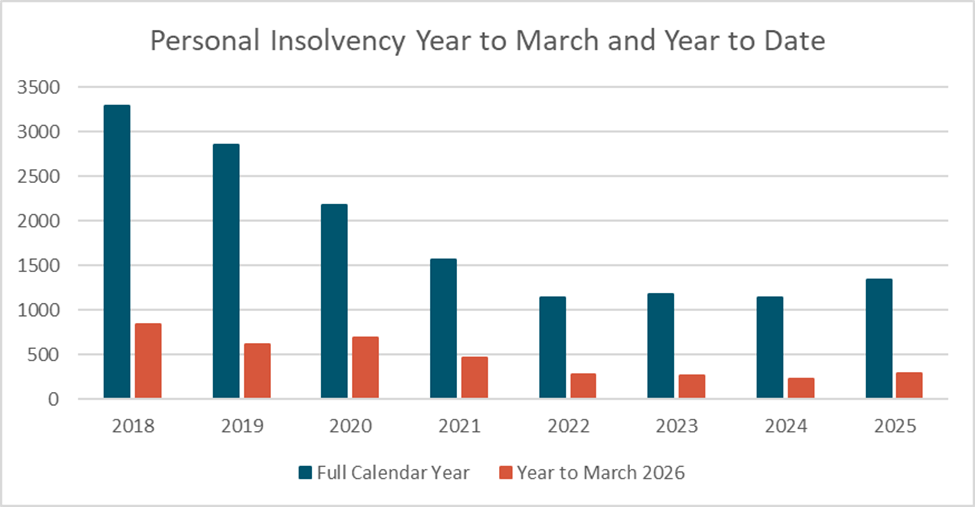

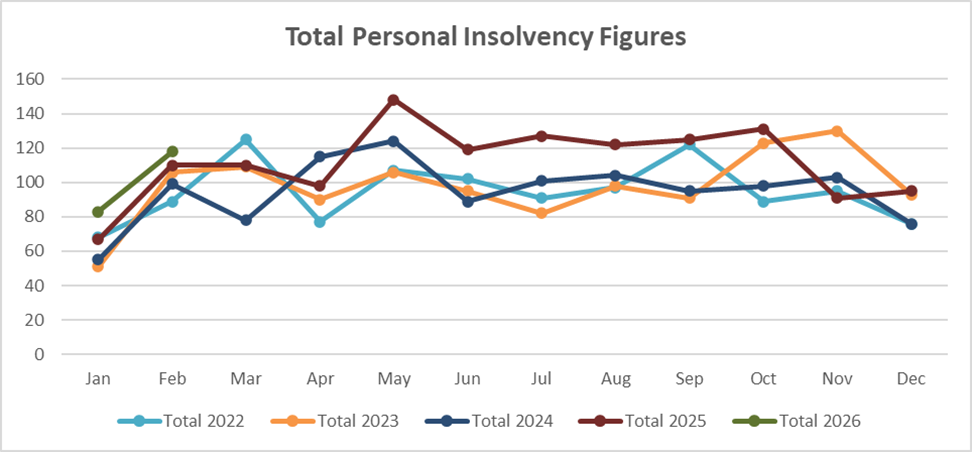

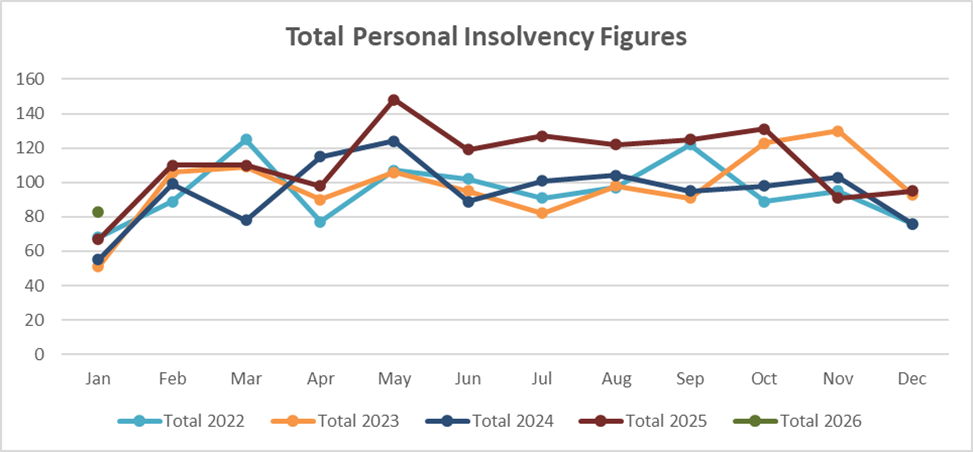

March saw more of the same on the personal insolvency front with little change. At this point we continue to expect more of the same with only minor rises and drops.

Where to from here?

After a big first third 2026 looks to be another big year unless something drastically changes. The stresses on the economy are not going away.

If you want to have a chat about any points raised or an issue you may have you can call on 0800 30 30 34 or email This email address is being protected from spambots. You need JavaScript enabled to view it..

11 May 2026

In New Zealand there is a critical window following the service of a winding up (“liquidation”) application on a company’s registered office. Practitioners commonly refer to this as the “10 working day rule” a practical and strategic timeframe that can significantly affect a company’s ability to control who is appointed as its liquidator.

This article explains the rule, its legal foundation, and its implications in practice.

Overview of the Rule

Once a winding up application is served on a company, the company has 10 working days in which it can still appoint its preferred liquidator (typically via shareholder resolution) without needing the consent of the applicant creditor.

After the 10 working day period expires:

- The company loses its unilateral ability to appoint a liquidator of its choosing.

- Any voluntary appointment requires the consent of the applicant creditor

Why the 10 Working Day Period Matters

Preservation of Shareholder Control

During this initial 10 working day window the company’s shareholders retain full control over the appointment of a liquidator. They can act quickly to appoint a practitioner of their choosing.

Shift in Control After 10 Working Days

Once the period expires the creditor who filed the winding up application gains procedural leverage. A voluntary liquidation initiated by the company is dependent on the creditor agreement. At this stage creditors may prefer their own nominee liquidator they have lined up rather than the one selected by the shareholders. The creditor may agree to the shareholders liquidator in situations where the practitioner is known to them or they did not have one lined up, it will allow for the company to be placed into liquidation earlier that having to wait for the court date and may reduce costs.

If a liquidator is subsequently appointed without the consent of the creditor they will be removed from the appointment and deemed to be invalidly appointed.

Practical Implications for Directors and Advisors

Urgency of Decision-Making

The 10 working day period is strategically critical. Directors must:

- Obtain insolvency advice quickly once served, ideally before this

- Assess solvency and alternatives (e.g. restructuring vs liquidation)

- Decide whether to appoint a liquidator voluntarily

Delay can result in:

- Loss of control

- Increased creditor involvement

- More complex and potentially adversarial proceedings

Tactical Considerations

Appointing a liquidator within the 10 working day window may:

- Avoid Court costs associated with the application

- Allow the company to nominate an experienced or preferred practitioner

- Demonstrate cooperation with creditors

Conversely, failing to act within the timeframe may:

- Lead to a creditor-driven liquidation

- Reduce flexibility in managing creditor relationships

Role of the Applicant Creditor

After the 10 working day period:

- The applicant creditor’s influence increases materially

- They may insist on their nominated liquidator

- A late voluntary appointment will be deemed invalid

This shifts the dynamics from company-led to creditor-driven decision-making.

Summary

The “10 working day rule” is a crucial feature of New Zealand insolvency practice:

- It begins upon service of a winding up application

- It provides a limited window for the company to appoint its preferred liquidator

- After expiry, control shifts toward the applicant creditor and the Court

For directors and advisors, the key takeaway is simple:

Act quickly within the 10 working day window if you want to retain influence over the liquidation process.

11 May 2026

Over the past 12-18 months, many New Zealand businesses have been navigating what can best be described as a “slow squeeze.” It hasn’t been a single catastrophic event, but rather a steady accumulation of pressures, these include rising interest rates, increased input costs, tighter consumer spending, and delayed payments.

For professional advisers working closely with clients, the challenge is recognising when normal trading stress crosses the line into genuine insolvency risk and knowing what to do next.

From Pressure to Distress: The Warning Signs

In our experience, business failure is rarely sudden. Instead, it follows a familiar pattern. Early recognition is key to preserving options and protecting outcomes.

Some of the more common early indicators include:

- Persistent cash flow shortages despite profitable trading on paper

- Increasing reliance on creditor stretching (especially IRD or trade creditors)

- Inability to meet tax obligations as they fall due

- Use of short-term funding (overdraft, credit cards, online loans) to cover structural deficits

- Mounting aged receivables with little prospect of recovery

At this stage, many business owners remain optimistic and focused on “turning things around.” The classic she’ll be right attitude NZers are known for. While that mindset is understandable, delay can materially worsen the position for all stakeholders.

The Critical Shift: Directors’ Duties Come Into Focus

Once a company is, or is likely to become, insolvent, directors’ obligations shift. The focus moves away from shareholders and toward creditors.

Continuing to trade while incurring debts that the company cannot realistically repay can expose directors to personal liability. This is an area that has seen increasing attention in New Zealand courts, and it’s something advisers should be proactively discussing with their clients.

It’s not about forcing a business to stop trading prematurely it’s about ensuring decisions are made with clear awareness of the financial position and associated risks and documented correctly.

Why Early Advice Leads to Better Outcomes

One of the biggest misconceptions is that engaging an insolvency practitioner means “the end of the road.” In reality, early engagement often creates more options, not fewer.

Depending on the circumstances, those options might include:

- Informal restructuring: Working with creditors to realign payment terms

- Refinancing or capital injection strategies

- Orderly wind-downs that preserve value and minimise losses

- Formal insolvency processes such as voluntary administration or liquidation, where appropriate

The earlier these conversations happen, the more control directors and advisers retain over the process, they may then plan and the better the likely outcome for creditors.

The Role of Trusted Advisers

Accountants and lawyers are often the first to see the signs. You’re in the numbers, the agreements, and the day-to-day reality of your clients’ businesses.

This places you in a powerful position but also creates a challenge. Raising insolvency concerns can feel uncomfortable, particularly when long-standing relationships are involved.

However, experience shows that clients are generally grateful for early, pragmatic guidance, even when the message is difficult. Framing the conversation around preserving value and protecting stakeholders can help shift the perception from “failure” to “management.”

Common Pitfalls to Avoid

When businesses get into trouble, we frequently see a few recurring mistakes:

- Waiting too long: Hoping trading conditions will improve often leads to a worse outcome

- Selective creditor payments: Prioritising some creditors over others without a clear strategy can create legal risk

- Poor record-keeping: Inadequate financial information makes it harder to assess options and defend decisions

- Avoiding communication: Silence with creditors tends to escalate issues rather than resolve them

Avoiding these pitfalls can significantly improve the position for all involved.

Final Thoughts

Tough trading environments are a normal part of the economic cycle, but the current conditions are testing many businesses that might previously have been considered stable or have never been through a downturn before.

For advisers, the opportunity lies in helping clients act early, make informed decisions, and avoid the compounding effects of delay.

If nothing else, the key message is simple: when it comes to financial distress, time is not neutral. Acting sooner almost always leads to a better outcome.

1 April 2026

Winding Up Applications

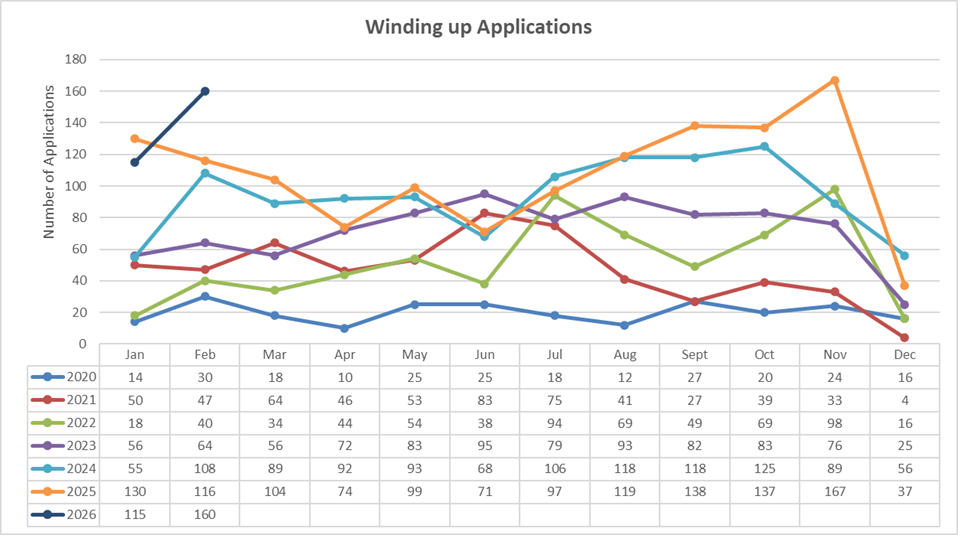

There will be a few instances of this saying in this article but for the first quarter of 2026 we have had the highest first quarter in the last 10 years. Comparatively we have had more winding up applications in 3 months than we had in all of 2020.

Businesses remain under the pump, with factors both inside and outside their control (war, fuel prices etc.) negatively affecting their bottom line and putting on the squeeze. Unfortunately, when this has happened in the past and when it inevitably happens again companies tend to step paying “The Bank of IRD” first. This in turn leads to the IRD debt growing and IRD taking more enforcement action driving winding up applications.

March had 90 applications for the month down on both January and February but this is a normal occurrence for March.

The IRD applications in March made up 66 of the 90, which is above their comparative march months from prior years. The drop-in appointments that put us below 2025 for March was from all other creditors chasing debts. Likely a combination of how the public holidays fell, growing uncertainty for businesses in the strength of the economy, along with the end of financial year and matters being put on the back burner for more important matters to be resolved before 31 March rolled around.

In March of 2025 there were 51 winding up applications in the month. In February 2026 all other creditors made up 48 applications, while in March 2026 they had dropped off to 24, so half.

2026 now looks like it may exceed 2025 if the first quarter is anything to go by. However, it is still early days to predict this in a year where the country goes to the polls. There remains a lot of pressure and uncertainty in the economy.

We remain a few months out from when we will get the next update from IRD on their current tax debt levels but at 30 June 2025 there was $9.3 billion outstanding. My prediction are on this growing to over $10 billion.

Company Insolvencies – Liquidations, Receiverships, and Voluntary Administrations

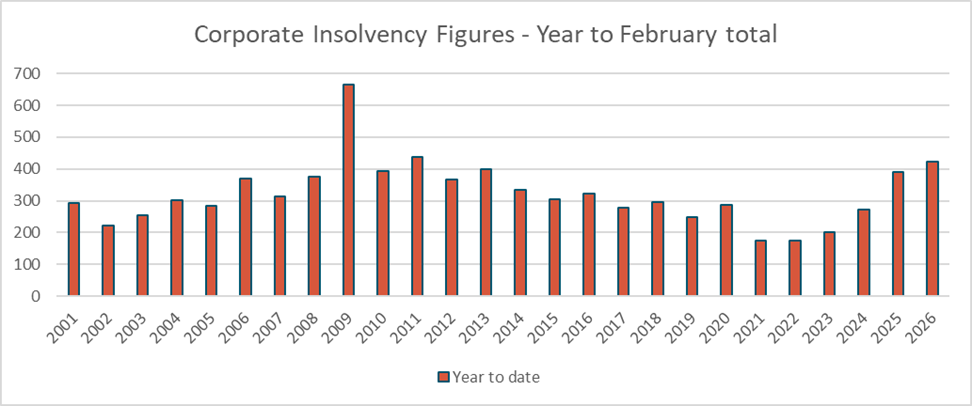

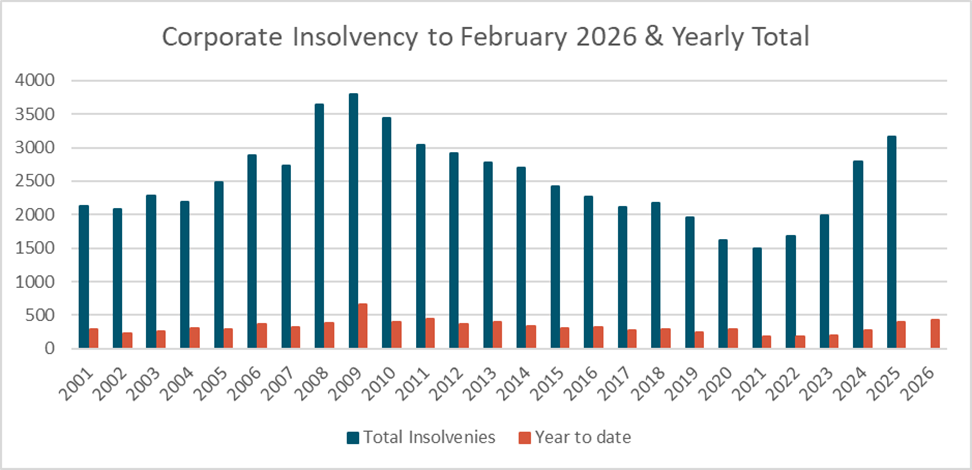

January, February and March 2026 has been the highest first quarter in the last 15 years for corporate appointments. Add to that October, November and December 2025 and you have been the highest rolling 6 months same time frame.

Corporate insolvency appointments in March 2026 continued the trend of coming in above their previous comparative months. So far, the first 3 months of 2026 is looking in line with what we saw in 2011 post GFC.

Solvent liquidations were around their historical March levels as stakeholders sought to squeeze them in before the end of the financial year. While insolvent shareholder liquidation and court liquidations were both 1.5x their long-term average in March.

We are still 6 months + out from November where people will start to take the wait and see approach but signs are pointing to a busy 2026 for insolvency practitioners off the back of a busy 2025.

With another month of elevated levels of court applications to wind up the number of court liquidations is expected to remain high.

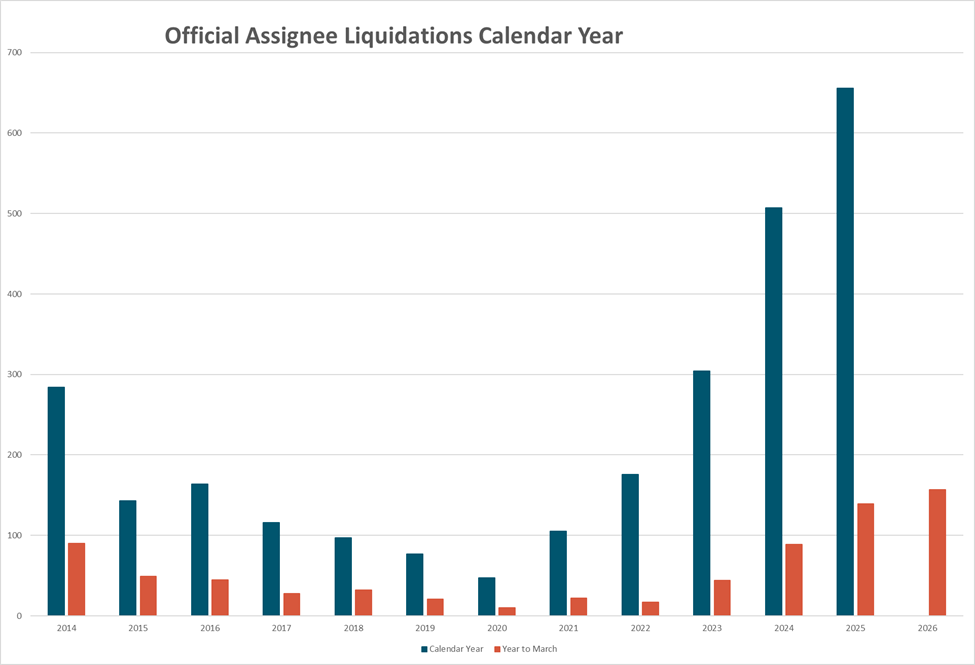

The Official Assignee took 60 liquidation appointments in March, almost all of them were IRD court applications. They continue to be the busiest liquidator in the country and have also had a bumper first quarter.

Personal Receiverships

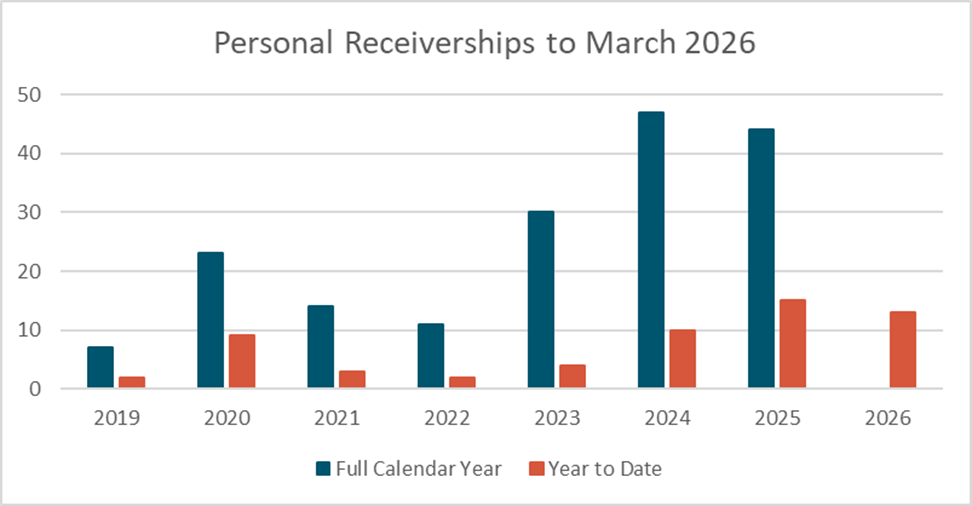

After a slow start to the year for personal receiverships when compared to 2025, March 2026 finally saw a jump with 8 out of the 13 appointments in the first quarter being appointed in March.

The uptick in Personal receiverships seen since 2024 is driven by the preference of some lenders towards obtaining a personal general security agreement from individual borrowers which allows them to appoint receivers upon default, rather than the traditional approach used by the bulk of lenders of relying on the often slower to enforce, personal guarantee to recover their debts.

Because there are no publicly available reports on the result of the receiverships, there is no register for individuals it is difficult to see how successful the appointment may be and if any funds are recovered along with what the costs involved were on each appointment. Alternatively, they may be acting as a fishing expedition to allow lenders a look into the individuals personal affairs to see what is behind the curtain and not searchable on the register.

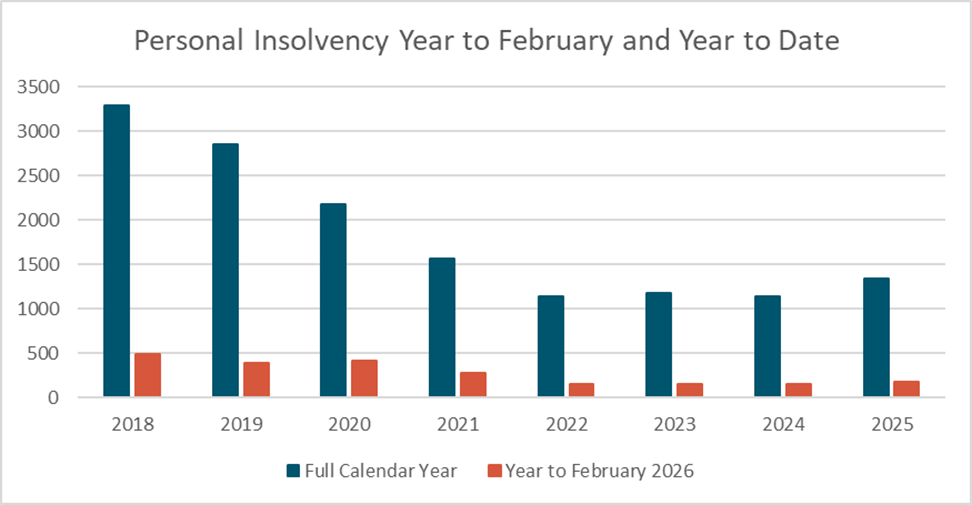

Personal Insolvencies – Bankruptcy, No Asset Procedure and Debt Repayment Orders.

February 2026 had 87 bankruptcies, of these 54 were through the courts, quite the jump from previous months but still only a minor lift from past years and not a definitive sign that bankruptcy figures have changes and are on the rise.

At this point we continue to expect more of the same with only minor rises.

Where to from here?

After a big first quarter 2026 will be an interesting year with the public at the polls in November, based on 2024 and 2025 insolvency figures appointments should continue to track up and look to be even higher than what we saw in 2025.

If you want to have a chat about any points raised or an issue you may have you can call on 0800 30 30 34 or email This email address is being protected from spambots. You need JavaScript enabled to view it..

14 April 2026

Liquidation is commonly misunderstood as something that only happens when a business has failed to pay its creditors. While creditor pressure is certainly one pathway to liquidation, it is far from the only one.

In practice, many liquidations arise from non‑financial or non‑creditor driven factors. These situations often involve people, strategy, risk management, or changes in circumstances rather than mounting arrears. Understanding these scenarios is important for directors, shareholders, and advisers, as early and informed decisions can preserve value and reduce risk when it does become time to consider liquidation as an option.

Below are some of the most common situations where liquidation is not driven by creditor action that we see.

Shareholder or Director Disputes

One of the most frequent non‑creditor reasons for liquidation is an irreconcilable dispute between shareholders or directors.

This is particularly common in:

- 50/50 ownership structures

- Family businesses due to divorce, generational conflict, or succession failure

- Companies without clear shareholder agreements or dispute resolution mechanisms

Often times parties enter into business ventures with rose tinted glasses thinking everything will work out, unfortunately down the line if decision‑making becomes paralysed or trust breaks down, the business can no longer be managed effectively even if it remains solvent. In these cases, liquidation may be the most practical way forward and bring matters to a close for the parties.

Deceased Estates

Liquidation may also arise following the death of a shareholder or founder. This is often common in sole director / sole shareholder companies.

Common challenges include:

- Shares passing to an estate with beneficiaries and executors who have no involvement in the business and no ability to run it

- Disagreement between surviving shareholders and the estate

- No succession plan or buy‑sell agreement in place

Where these issues cannot be resolved commercially, liquidation can provide a fair and transparent mechanism to realise assets and distribute value. This option becomes one that can be acted on quickly when the business is continuing to trade and employs staff, this gives staff certainty on what will happen moving forward and next steps to either close the business or aim to sell it as a going concern.

Loss of a Key Person

Many businesses are heavily dependent on one or two individuals often the founder or a senior operator who have worked in the business for years.

When a key person is lost due to:

- Death

- Serious injury or illness

- Burnout or retirement

the business will struggle to continue The loss of the customer base they may represent, knowledge and know how can be crippling for the business, even if it has historically been profitable.

In these circumstances, liquidation is not a failure it is a recognition that the business cannot operate as originally structured and that winding up in a controlled manner is preferable to drifting into financial distress.

Loss of a Key Client or Contract

Some businesses rely on a small number of major clients or a single cornerstone contract.

If that relationship ends, the business may:

- Remain solvent

- Have no immediate creditor pressure

- But lack a sustainable future

Rather than trading on in the hope of replacement work, directors may choose liquidation as a proactive step to minimise risk and protect stakeholders. This is often times a pivot point where stakeholders realise they are ready to cash up and move on to new pursuits.

Strategic or Commercial Decisions

Liquidation is sometimes the result of a deliberate strategic decision rather than financial failure.

Examples include:

- A business model that no longer stacks up due to market changes or a sunset industry

- Margin erosion that makes future trading unattractive

- Increased regulatory or compliance costs

- Legislation changes making the business no longer viable

- Inability to sell the business as a going concern

In these cases, liquidation can be the most efficient way to realise remaining value and exit cleanly.

Proactive Risk Management

Experienced directors often use liquidation as a risk‑management tool, not a last resort.

This can include situations where:

- The business is still meeting its obligations but future risks are increasing

- Personal guarantee exposure is escalating

- Litigation or contingent liabilities are emerging

- External and internal funding support is becoming uncertain

Choosing to stop early can significantly reduce personal and corporate exposure.

Group Simplification and Structural Reasons

Liquidation can also arise from corporate housekeeping rather than trading distress.

Examples include:

- Redundant entities within a group structure

- Special purpose vehicles that have completed their role

- Historic companies with no ongoing purpose

- Where insurance enables solvent liquidation rather than a workout

In these circumstances, liquidation is a practical way to formally close down an entity and ensure statutory obligations are met, it also allows you to avoid the ongoing compliance costs of keeping the company in the register.

Liquidation Is Not Always Failure

The common thread in all of these scenarios is that liquidation is not necessarily about unpaid creditors or business collapse. Often, it is about:

- Control

- Certainty

- Risk reduction

- Closing a chapter properly

When approached early and handled correctly, liquidation is a useful option allowing you to make a commercial, orderly, and responsible decision.

If you are facing structural, strategic, or people related challenges in a business, seeking advice early is critical. Understanding your options may preserve value and prevent unnecessary risk.

14 April 2026

From a liquidator’s perspective, non‑registration or defective registration on the Personal Property Securities Register (“PPSR”) remains one of the most common reasons creditors lose priority and, in many cases, recover nothing in an insolvency.

In most insolvency appointments, one of our early tasks is to determine the priority of competing claims over company assets. That exercise is heavily influenced by PPSR registrations. Where a creditor has failed to register, or cannot support a registration with enforceable documentation, the outcome is often commercially severe and entirely avoidable.

Security Interests Apply to More Arrangements Than Many Businesses Realise

Despite the Personal Property Securities regime having been in place for well over 25 years, many businesses remain unaware that it applies to a wide range of ordinary commercial arrangements, including:

The supply of goods on retention of title terms

Leases of goods for more than one year (or for an indefinite term)

Consignment stock arrangements

In each of these scenarios, creditors frequently assume their ownership rights or contractual terms protect them. In a liquidation, however, those assumptions can carry little weight unless the security interest has been validly created and properly registered on the PPSR.

Registration Alone Is Not Enough

A recurring issue for businesses placed into liquidation and receivership is creditors who have either not registered at all, or who have registered but cannot produce documentation that legally supports the claimed security interest.

Valid and enforceable terms and conditions of trade, signed lending and loan documentation or financing agreements among others, with registration of a Financing Statement on the PPSR, are essential if a creditor expects to recover goods or the proceeds of sale of those goods. One without the other often provides little practical protection.

It is common for liquidators to encounter PPSR registrations that:

Are unsupported by any signed or agreed security agreement

Do not accurately reflect the terms relied upon

Contain errors in debtor details or collateral descriptions

In such cases, the registration may be ineffective and disregarded when determining priority.

Priority Is Determined Strictly

When distributing assets, liquidators must apply the Personal Property Securities Act. There are often multiple competing security interests over the same assets some valid and perfected, others not.

Creditors who have correctly created and registered their security interests will generally gain priority over unsecured creditors and, in some cases, over other secured parties when there are multiple valid secured parties the timing of registration becomes important. Those who have not are typically relegated to the unsecured pool is there is a shortfall from the sale of the asset.

For example, a supplier with a valid retention of title clause / specific security who has registered that interest on the PPSR will usually rank ahead of a General Security Agreement (“GSA”) holder and preferential creditors in regard to the specific secured assets. Without registration, the retention of title clause is generally ineffective, and the supplier will rank behind the GSA holder and preferential creditors frequently resulting in no recovery.

A Persistent and Costly Mistake

Despite the maturity of the PPSR regime, we continue to routinely encounter situations where creditors have failed to register security interests associated with leases or retention of title arrangements. In many cases, the absence of a registration directly results in the creditor losing priority and recovering nothing.

From a liquidator’s perspective, these outcomes are neither unusual nor unexpected they are the natural consequence of failing to comply with the PPSR framework.

Cost Versus Consequence

The cost of PPSR registration remains minimal when compared with the potential consequences of non‑registration. As at the time of writing (April 2026), the fee to register a Financing Statement is $16.10 (including GST). By contrast, we frequently see creditors lose claims worth many thousands of dollars simply because a registration was not made, was incorrectly completed, or was not supported by enforceable documentation. This seems a waste for the potential saving of $16.10. Creditors do not need to register every individual supply to a customer on the PPSR, one valid registration will cover the account and is renewed every 5 years.

A Final Observation from a Liquidator’s Perspective

In an insolvency, outcomes are not determined by commercial fairness, historical relationships, or what the parties believed was agreed. Priority is determined by legislation that requires the existence of a valid security interest, proper PPSR registration, and accurate supporting documentation.

Creditors who attend to these matters early place themselves in a much stronger position if their customer becomes insolvent. Those who do not often only become aware of the importance of the PPSR once it is too late to fix.

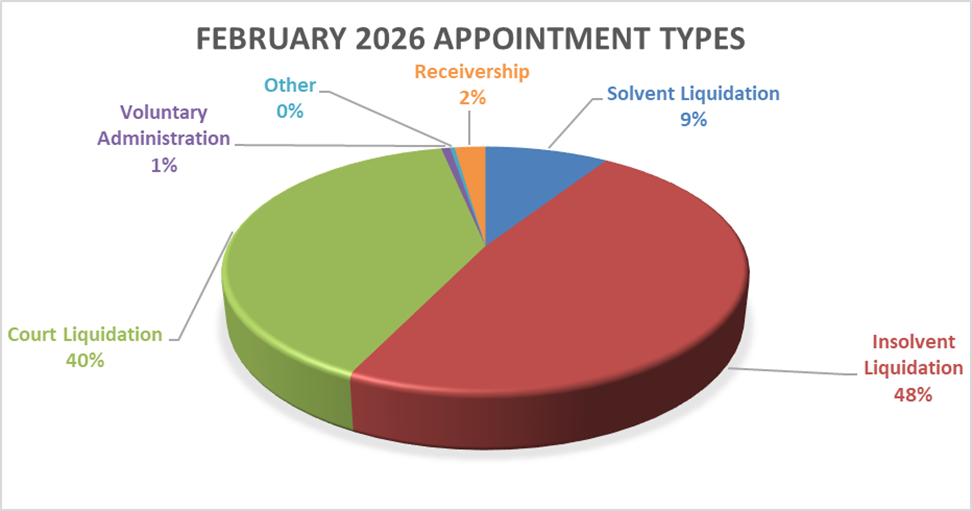

Insolvency by the Numbers #62: NZ Insolvency Statistics February 2026

What have the insolvency numbers done in February 2026, we also look at what could be instore for the rest of the 2026 for personal and corporate insolvency.

Winding Up Applications

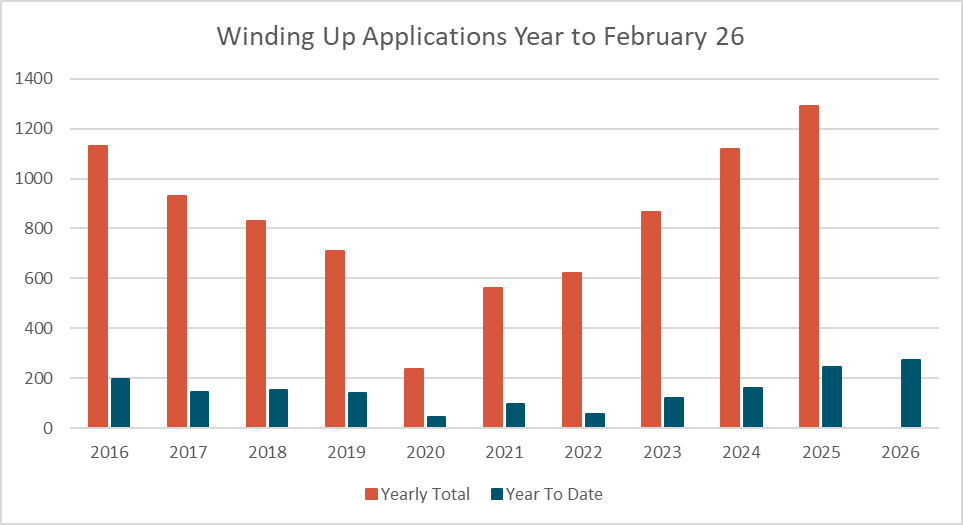

We have started off the year with a bit of pressure seen in the number of winding up applications advertised, it has exceeded what we saw in 2025.

Businesses are still under the pump, and it is being driven by the IRD in large part making up 193 of the 275 January and February winding up applications.

February had 160 applications advertised making up for the slightly slower start seen in January 2026. February 2026 was the 2nd highest month for total appointments over the last 10 years with only the 167 applications seen in November of 2025 exceeding it.

The IRD applications in February made up 112 of the 160, coming in 2nd again only to November 2025 where they advertised 127 appointments in the month.

A big month for winding up applications and it will flow through into a big March and April for appointments through the courts as pressure on delinquent debtors continues to grow.

2026 looks like it will exceed 2024 an off the back of February potentially 2025. However, it is very much still early days to predict this particularly in an election year There remains a lot of pressure in the market with higher than desired inflation, no further drops in the OCR likely, and war likely influencing businesses cost margins as fuel price shocks flow through the supply chain and create additional uncertainty.

Company Insolvencies – Liquidations, Receiverships, and Voluntary Administrations

February 2026 continued the January trend coming in above the comparative months in 2025 it is looking like LIP’s will be in for another busy year. Appointment figures are still down on the GFC figures but are in line with wat was experienced in the shoulder years of 2010 and 2011.

With another month of high levels of winding up application the number of court appointed liquidations is expected to remain high currently sitting at 40% compared to its long-term share around 27%.

The Official Assignee took 95 liquidation appointments in February, almost all of them were IRD court applications. They continue to be the busiest liquidator in the country taking more in one month than a lot of practitioners take in one year.

Personal Insolvencies – Bankruptcy, No Asset Procedure and Debt Repayment Orders.

Personal insolvency figures saw a lift in January when compared to the same month in the last few years but it was not a noticeable jump.

Comparatively they took 44 bankruptcies in January but have on average in 2025 taken 55 liquidations per month with highs of 105 in some months.

At this point we continue to expect more of the same for the first half of 2026 as we head into the election.

Where to from here?

2026 will be an interesting year with an election in the tail end, based on 2024 and 2025 insolvency figures appointments should continue to track up and look to be even higher than what we saw in 2025.

The economy is by no means in the free and clear and has some rough time ahead on the way to recovery. How this plays out with the wait and see approach people take in an election year means the pain may be prolonged and pushed out into 2027.

As always its better to take action and act early, it will often get a better result for all stakeholders.

If you want to have a chat about any points raised or an issue you may have you can call on 0800 30 30 34 or email This email address is being protected from spambots. You need JavaScript enabled to view it..

1 March 2026

As licensed insolvency practitioners, our principal duty under section 253 of the Companies Act 1993 (copied at end of article) is to take possession of, protect, realise, and distribute assets to creditors in a reasonable and efficient manner. This statutory obligation sits at the core of how McDonald Vague operates and guides our approach on every appointment.

In practice, this means returning funds to the people and organisations who rely on them most employees awaiting wage and holiday pay arrears, small business owners needing overdue funds to stabilise cashflow, and the IRD chasing their tax arrears. Ensuring meaningful distributions is central to our role and a key measure of effective insolvency administration.

Our ability to make distributions at scale stems from our experience in identifying, recovering, and realising assets across a wide range of situations, supported by efficient processes and responsible fee management, a longstanding focus of the firm.

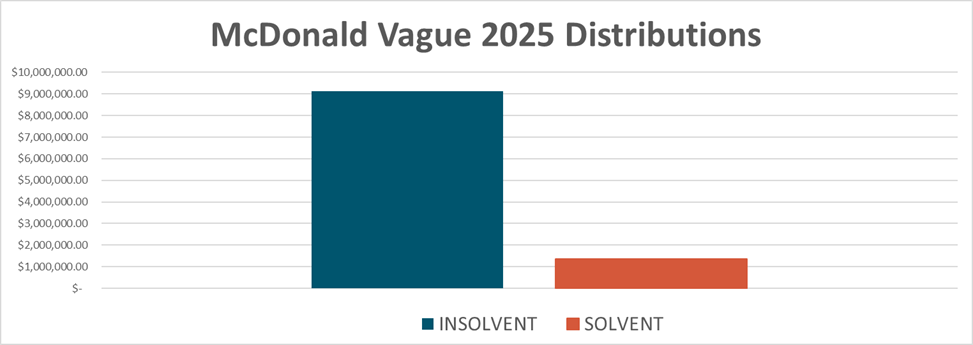

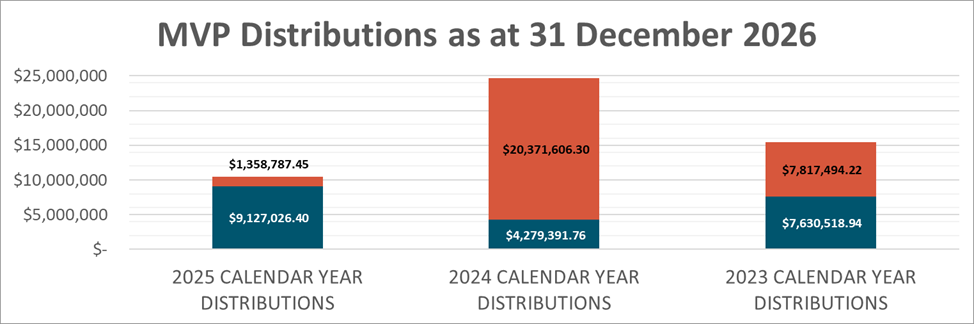

2025 Distribution Summary

Across all insolvent and solvent appointments concluded within the 2025 calendar year, McDonald Vague paid out a total of:

Insolvent Appointments: $9,127,026.40

Solvent Appointments: $1,358,787.45

These results reflect consistent performance across our portfolio rather than reliance on any single appointment.

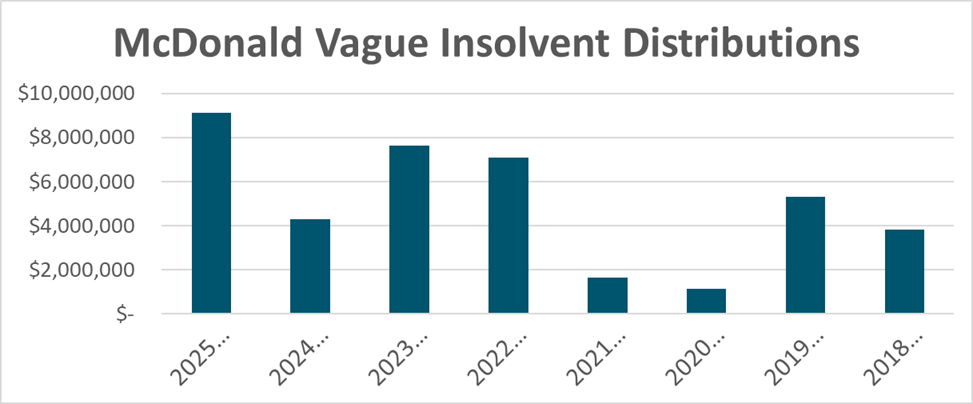

Insolvent Company Distributions

In 2025, a total of $9,127,026.40 was distributed to creditors in insolvent company liquidations. These distributions were made across 56 separate appointments, demonstrating diversification of recoveries and steady throughput of work across the year.

The breakdown of these distributions is as follows:

Preferential Creditors: $547,455.30

Secured Creditors: $6,137,593.50

Unsecured Creditors: $2,441,977.60

Returning funds to unsecured creditors often the group with the least expectation of recovery continues to be a point of pride for our team.

Solvent Liquidation Distributions

Solvent liquidations also formed part of our 2025 workstream, delivering $1,358,787.45 back to shareholders across various appointments.

Solvent liquidations remain an efficient and legally robust mechanism for companies that have completed their purpose and can pay all liabilities within 12 months — a process we regularly support for business owners undertaking restructuring, group simplification, or succession planning.

Our Ongoing Focus

As one of New Zealand’s leading insolvency and business recovery firms, our emphasis remains on:

Maximising creditor returns

Responsible fee management

Efficient realisation and distribution of assets

Clear, practical communication with stakeholders

Each distribution reflects the practical value we deliver to creditors, business owners, and the wider commercial community.

If you would like to discuss any aspect of the 2025 results or require advice on an appointment, our licensed insolvency practitioners are available to help.

Section 253 of the Companies Act 1993 sets out:

“Duties, rights, and powers of liquidators

253 Principal duty of liquidator

Subject to section 254, the principal duty of a liquidator of a company is—

(a) to take possession of, protect, realise, and distribute the assets, or the proceeds of the realisation of the assets, of the company to its creditors in accordance with this Act; and

(b) if there are surplus assets remaining, to distribute them, or the proceeds of the realisation of the surplus assets, in accordance with section 313(4)—

in a reasonable and efficient manner.” – emphasis added

1 March 2026

In situations where PAYE has been deducted from wages but not paid to Inland Revenue, directors and associated persons of close companies may face unexpected personal tax consequences. Inland Revenue has the ability under Section LB 1(3) of the Income Tax Act 2007 to reassess an individual’s tax return and limit their PAYE tax credits to the amount actually received by the Commissioner. Given the number of liquidations we manage where PAYE arrears are present, it is important that directors understand this rule. The article below explains how the section operates and why Inland Revenue may invoke it.

Section LB 1(3) — Income Tax Act 2007

We want to take this opportunity to draw your attention to a lesser‑known or used section of the Income Tax Act 2007 (ITA 2007) that we have seen applied by the Inland Revenue (IRD) in some recent liquidations. The section, however, can be used in other situations when PAYE has not been paid to the IRD by an employer.

We think it is important that directors and advisors are aware of this section where directors and/or associated persons are being paid on the payroll of a close company(1) (all or part of their remuneration) and having PAYE deducted, that when the employer does not pay (or is contemplating not paying) the PAYE to the IRD.

Section LB 1(2) of the ITA 2007 allows a tax credit for the tax year equal to the amount of tax withheld from a PAYE income payment of a person who is an employee.

Section LB 1(3) of the ITA 2007 limits this credit to the amount of tax paid by the employer to the Inland Revenue if certain conditions are met.

This section allows the IRD to reassess the income tax return of a director or shareholder if the amount of the tax credit is more than the amount of tax paid to the Commissioner if

(a) the employer is a close company(1); and

(b) the employer and the person are associated persons, or the employer and the spouse, civil union partner, or de facto partner of the person are associated persons; and

(c) the employer withheld the amount of tax for the PAYE income payment shown in their employment income information.

In a liquidation, this section is not something the Liquidator has any control over as it impacts the individual taxpayer and relates to events before the Liquidation. This is a section the IRD can apply at its discretion to the individual taxpayer.

A Simple Example

A is a director/employee who has been paid $150,000 during a tax year and $42,414 tax had been reported as PAYE deducted at source through Payday filing.

The company still owes $20,000 of this amount in unpaid PAYE.

The IRD can reassess A’s tax return to reflect only the $20,000 having been paid against their earnings, making them personally liable for the shortfall in tax due.

While Section LB 1(3) is technical in nature, its impact can be significant for directors and associated persons when PAYE has been withheld but not paid. Importantly, this is a matter that Inland Revenue deals with directly with the taxpayer and sits outside the liquidator’s control. Directors and advisors should therefore be mindful of PAYE arrears as they arise, as the consequences can extend beyond the company and into an individual’s personal tax obligations.

Definition

(1) Close company:

A company that has five or fewer natural persons (associated persons counted as one) who either hold voting interests, or hold market value interests in the company of more than 50%.

Reference

Section LB1 of the Income Tax Act 2007 can be found at:

https://www.legislation.govt.nz/act/public/2007/0097/latest/DLM1517915.html

Insolvency by the Numbers #61: NZ Insolvency Statistics Year End 2025 and January 2026

What have the insolvency numbers done in 2025 along with January 2026, at the same time we take a look at what could be instore for the rest of the 2026 for personal and corporate insolvency.

Winding Up Applications

Surprising no one based on how the first 11 months of 2025 were tracking we finished the year with 1289 winding up applications for the year, well above any of the past 5 years and reinforcing that we are yet to see the end of the pressure businesses are facing.

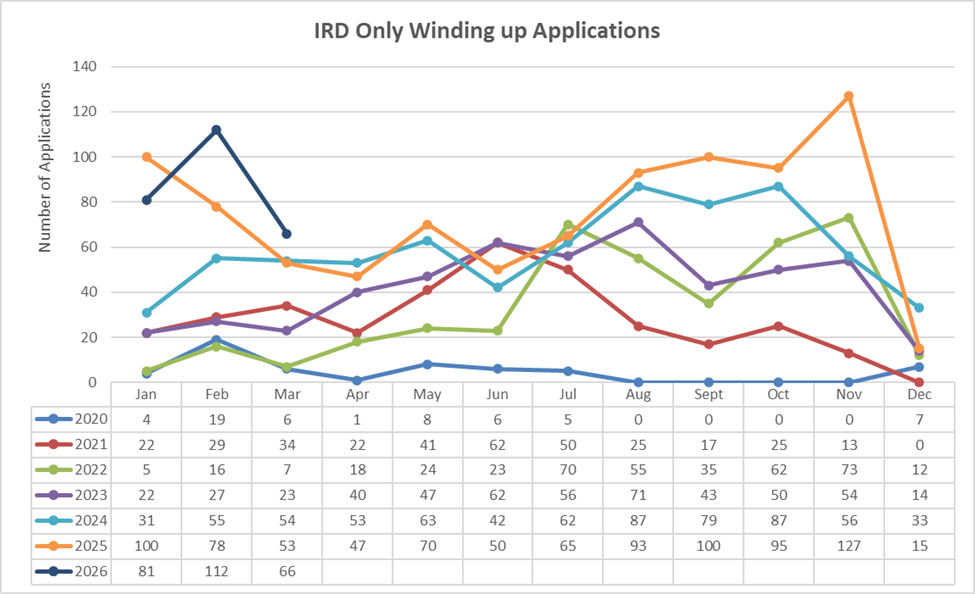

The January monthly total was 115 applications, slightly down on the 2025 total of 130 application. This drop was made up entirely of a reduction in IRD winding up applications from 100 in 2025 to 81 in 2026. Theses application all had February and March hearing dates, so we are expecting to have a busy 2 months to start the year from court appointments.

2026 looks like it will exceed 2024 but may not yet reach the highs of 2025. However, it is very much still early days to predict this.

The big question will be how the November election will play out, and what effect this will have on insolvency appointments. The incumbent government has set the date late in the year to give the economy as much time as possible to have some form of recovery. But with the IRD still sitting on billions of dollars of debt to collect in they may be hard placed to not pursue businesses for what they are owed. It’s a double-edged sword, IRD takes the pressure off and business owners feel less pressure but then the government doesn’t have the recoveries to funds the traditional election year lolly scramble. Whereas if IRD keeps the pressure on business confidence remains in the tank and the recovery takes longer. Its unlikely we will be seeing any further OCR drops with the official stats showing raises in inflation outside the target band and unemployment on the rise particularly in the lower age bands.

December 2025 was the first time in in 32 months where all other creditors applications amounted to more than those advertised by the IRD. I would be hesitant to read to much into this however due to the Christmas close down period December is traditionally a slower month for IRD winding up applications. If this had happened in any other month it may have been worth more of a mention.

The Auckland High Court dealt with more winding up applications than the rest of the country combined in 2025 700 applications vs 589 applications. That is a fair bit of creditor enforcement and a wide margin between Auckland and the rest of the country,

Being the largest city in NZ by population cap Auckland draws increased business numbers, there will in turn be increased business failures and increased creditor enforcement. Though by population cap Auckland is only 34.14%, making up 54.31% of the winding up applications is still a touch high.

Christchurch sits in the 2nd spot dealing with 116 applications vs 2024 where they say 87, overall, up from 7.79% of the total to 9.00%. Likely a reflection of the slowdown in building work in 2025 post rebuild and all the slowdown in new build developments happening in the region after a few big years of new homes.

Hamilton managed to leapfrog 2024's 3rd place holder Wellington, a combination of Hamiltons increase in applications and Wellingtons applications in 2025 dropping to 72 from 80 in 2024.

Tauranga and Rotorua fill out the top 5 in the same order as 2024.

Notably for the rest of the High Courts Whangarei saw a sizable increase going from 10 applications in 2024 to 36 applications in 2025.

Company Insolvencies – Liquidations, Receiverships, and Voluntary Administrations

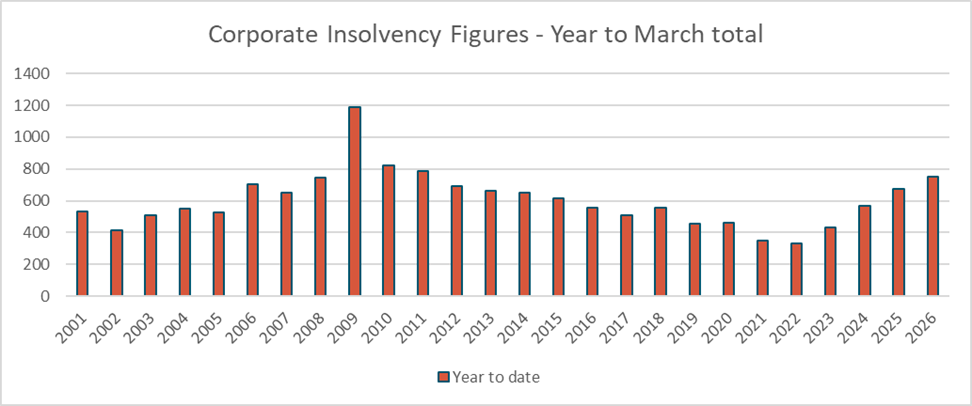

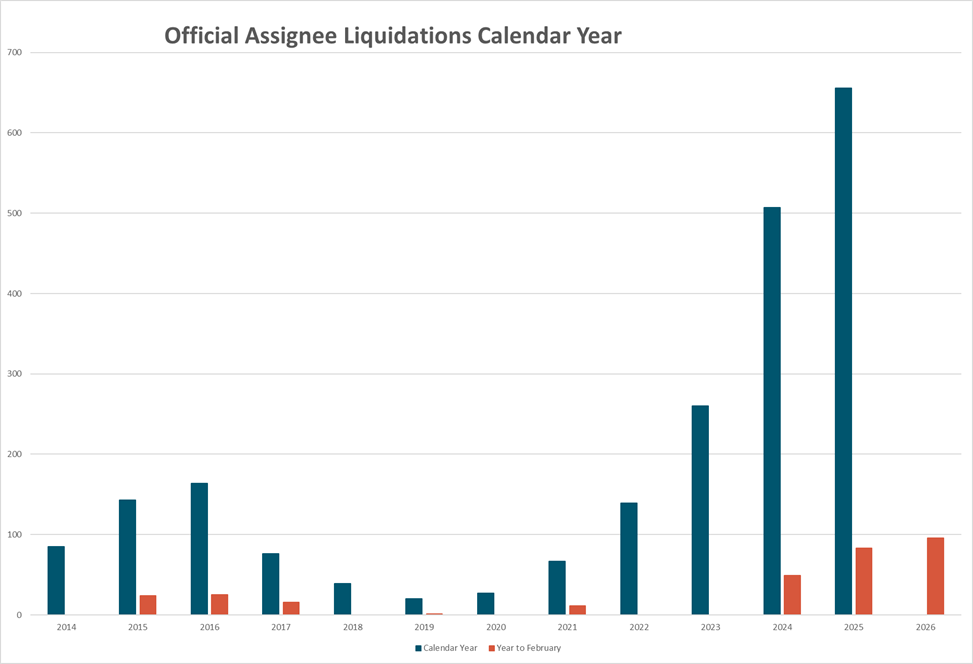

December 2025 finished out a strong year for corporate insolvency appointments, the months was slightly down in 2024 but overall, for the year it ended up around the totals from 2011. So, while a new high for recent years and above the 3,000 predicted last year it is still 600+ appointment down on the 2009 peak.

2025 3,163

2011 3,034

2010 3,438

2009 3,797

2008 3,645

January 2026 on the other hand took off with a hiss and a roar posting 114 appointments in a traditionally quitter month setting the scene for another busy year. While not quite at GFC levels again for January we are still right around the appointment levels seen in the 2009 shoulder years.

With the high levels of winding up application this month and towards the end of 2025 the number of court appointed liquidations is expected to remain high, however with the courts closed in January shareholder insolvent liquidations made up 84% or 96/114 total for the month with Receiverships and Solvent liquidations filling out the rest. Solvent liquidations continue to remain down on their average but we expect to see them pick up as we head into the end of the financial year.

The liquidations taken by the Official Assignee peaked in 2025 off the back of IRD winding up applications. In December 2025 the Official Assignee took 44 of the 76 court appointed liquidations. They continue to be the busiest liquidator in the country.

Personal Receiverships

Personal receiverships slowed in the final quarter of 2025 finishing out the year slightly down on 2024. This slowdown has carried through to January 2026 with only 1 new appointment in the month. As corporate insolvencies continue at elevated levels we expect this to pick up over 2026 as companies default the creditors come calling on the stakeholders that have provided security over their personal assets in order to recover something on their debt.

Personal Insolvencies – Bankruptcy, No Asset Procedure and Debt Repayment Orders.

Personal insolvency figures have remained stable at only slightly elevated levels for the 2025 year. When compared to the corporate insolvency levels the two have previously tracked along together while in the last 2 years corporate insolvencies have tracked up while personal insolvency has remained largely flat.

At this point we continue to expect more of the same for the first half of 2026 as we head into the election.

Year on year the 2025 figures were above the last 3 years, while on the increase they remain behind the 2021 figures. This period remains one of the lowest bases for personal insolvency figures.

Where to from here?

2026 will be an interesting year with an election in the tail end, based on 2024 and 2025 insolvency figures appointments should continue to track up. The economy is by no means in the free and clear and has some rough time ahead on the way to recovery. How this plays out with the wait and see approach people take in an election year means the pain may be prolonged and pushed out into 2027.

As always its better to take action and act early, it will often get a better result for all stakeholders.

If you want to have a chat about any points raised or an issue you may have you can call on 0800 30 30 34 or email This email address is being protected from spambots. You need JavaScript enabled to view it..